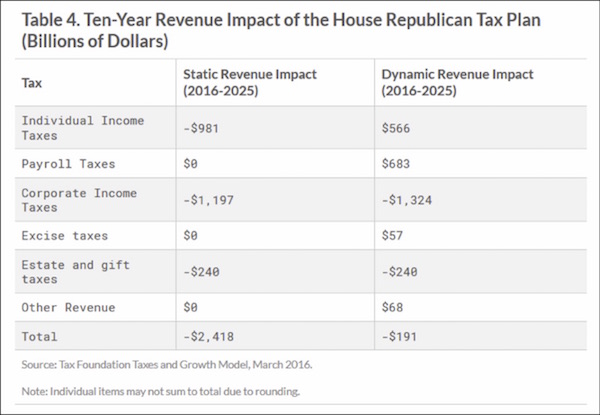

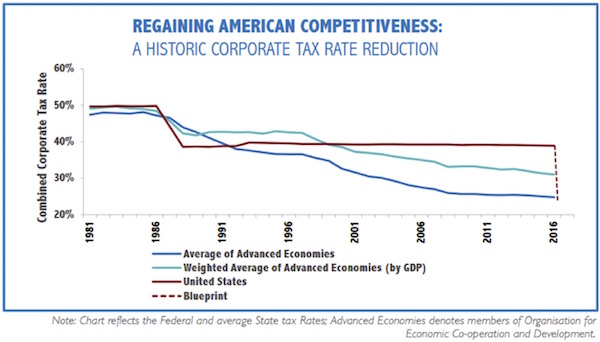

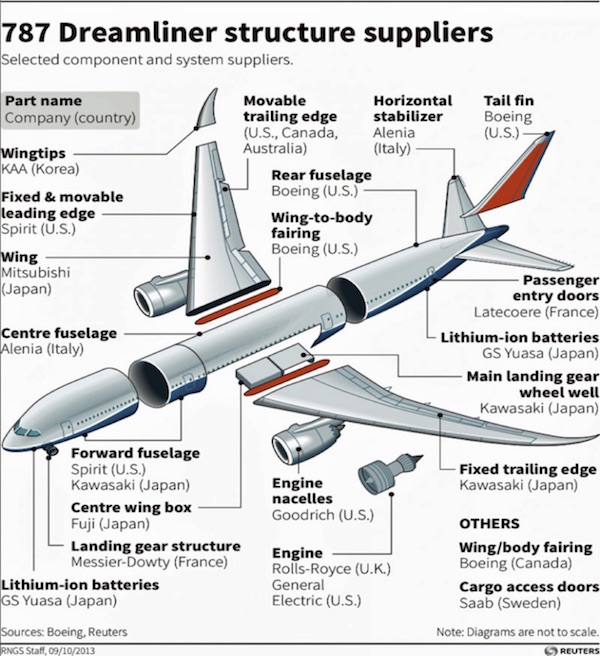

| By John Mauldin | Feb 19, 2017 Tax Reform: The Good, the Bad, and the Really Ugly—Part Three “We have a system that increasingly taxes work and subsidizes nonwork.” – Milton Friedman “You must be the change you wish to see in the world.” – Mahatma Gandhi “Real change requires real change.” – Former Speaker of the House Newt Gingrich Today we come to part 3 of my tax reform series. So far, we’ve introduced the challenge and begun to describe the main proposed GOP solution. Today we’ll look at the new and widely misunderstood “border adjustment” idea and talk about both its good and bad points. What follows may make more sense if you have first read part 1 and part 2. Next week we’ll explore what I think would be a far superior option, though one that is based on the spirit of the current proposal. If House leadership thinks they can get the present proposal through (doubtful), then they should stop messing around and do something really controversial by changing the entire terms of engagement. As my friend Newt Gingrich has often told me , “John, real change requires real change.” Warning: There is something in this series to offend almost everyone. Everything is fair game. If nothing else, I hope that no one can accuse me of simply talking the Republican book. I think this letter will pretty much eviscerate the key component of the proposed Republican tax plan. I hope the plan will be seriously changed. Many of you have direct contacts with your Senators and Representatives on both sides of the aisle. I urge you to send this letter to them and talk to them. This is one of the most serious national conversations we have ever had. We can all argue about how big government should be, but whatever we decide upon, we must pay for, if not through taxation then through a massive debt-deflationary depression or serious inflation. (Next week we’ll talk about how to avoid these problematic outcomes. Yes, it can be done.) It’s not a question of cost or no cost, it’s a matter of who will pay and how much. The question is how to allocate the cost efficiently, equitably, and with the least possible economic distortion. I have talked to many of the participants in the tax reform process, both in Congress and in think tanks. The one point of agreement is that the tax system must be massively reformed. That point, unfortunately, is where agreement ends. Tax reform ideas usually fail because the status quo gives everybody some kind of perceived benefit. In reality, the benefit may be worth less than people think, but it’s preferable to the uncertainty of a new system. This is basic game theory stuff, where the status quo is seen as what the economist types would describe as a “Nash equilibrium,” or a situation in where everybody has figured out how to make the system work for them, whether or not they are happy with it in toto. As long as nobody disturbs the equilibrium, things go on as they have done – until they don’t. The topic of equilibrium is one we’ve covered in past weeks, and we’ll be returning to it. Last week I described the tax reform ideas that House Speaker Paul Ryan and his caucus include in their “Better Way” blueprint. As I said, there’s a lot to like in their plan. There are parts of it I love. I am most enthusiastic about the pro-business/entrepreneurial encouragement they offer. Truly, we cannot resolve our national economic dilemma without growing the entrepreneurial and business side of our equation. One of the few things that the Paul Krugmans of this world and I agree on is that we must figure out how to grow our way out of the problems we face. However, we must remember that the “Better Way” is simply a set of proposals at this time. President Trump announced on Feb. 9th that his economic team is drawing up its own “phenomenal” business tax reform proposal. He said the White House would reveal it in the next few weeks. We have no idea whether it will resemble the House GOP plan. We do know the president hasn’t sounded enthusiastic about the border adjustment tax idea. We are also reading about major pushback on the BAT from many Senators and Congressmen. I’m not enthusiastic about the BAT either, to say the least. I fear it would come with serious macroeconomic side effects, and not just for the US. Cutting to the chase, when I say serious macroeconomic side effects, I am talking about its potentially triggering a global recession, which would mean a major bear market and a total reset of valuations in every asset class. Not the end of the world, but certainly not without pain and cost. Let’s pick up the story right there. Border Crossings Before I describe how border adjustment works, let’s note why it is part of the Republican plan. The features I described last week, while attractive to many taxpayers, also cut deeply into the government’s tax revenue. Here is how the Tax Foundation calculates the plan’s impact, under both static conditions and a dynamic model that tries to assess economic changes.  Under static conditions, the plan would reduce tax revenue by some $2.4 trillion over ten years. A dynamic scoring reduces that amount to $191 billion. The reality is probably somewhere in between, but no one really knows. I tend to lean toward the dynamic scoring, but the plan is still not revenue-neutral in a world where the US is already running nearly $1 trillion deficits. I give Chairman Brady and the House Republicans (who are constitutionally responsible for initiating tax proposals) an A+ for trying to avoid increasing the deficit and the national debt with their tax cuts, and without offsetting the cuts with tax increases somewhere else. Seriously, two thumbs up! Longtime readers know I am a deficit hawk, and I appreciate the budget-balancing intentions of my fellow Texan who is chairman of the Ways and Means Committee. However, the tax cut proposals we discussed last week mean that Congress must find new revenue to make up for them. The borde r adjustment tax (BAT) is their idea to help fill that gap. Here is how it works: Businesses that import goods from outside the US would not be able to deduct the cost of those goods from their corporate tax returns. But companies that export products to other countries would not count as income the revenue received from the exports. The hopeful effect of this measure is to encourage exports and discourage imports, which is in keeping with President Trump’s objectives. It also helps offset the proposed lower corporate income tax rates that bring the US more in line with other developed countries. However, the proposal also assumes that running a trade deficit is something the United States should try to avoid. There are serious pluses and minuses to that view. Most Americans may not realize how different our tax system is from those of every other country in the world. Almost every other nation has some variation of a value-added tax (VAT), a form of sales tax added at every level of production. Many also have corporate income tax, but the rates are lower than ours.  The House GOP plan (the red, dotted “Blueprint” line at the far right in the chart above) brings our corporate tax rates much closer to the average. Other countries make up the revenue gap with a VAT. The Better Way plan does it with border adjustment, which is sort of a halfway VAT. The problem is that the US runs an enormous trade deficit because our whole economy depends on imports. We do not presently have the capacity to replace those imports with domestic goods. Can we build that capacity? Yes, but not overnight. In the meantime, this plan would cause prices for everything imported to rise sharply (think a 20% increase on much of what you buy at Walmart or Amazon), or the importers will go out of business, or both. This is obviously not good for job creation if you are an importer. So what are the Republicans thinking? Why propose something that seems so daft? Well, in theory the BAT will bring in a lot of revenue, something like $1 trillion over 10 years if their assumptions are correct. This revenue is necessary to keep the Better Way plan’s other tax cuts from adding to the debt. And it will also theoretically increase jobs tied to exports. More on that below. The Republicans also pitch the BAT as simple fairness. Other countries apply their VAT taxes to goods shipped to the US, so the US should do likewise. The problem here is that the US doesn’t have a VAT, so we’re adjusting for something that doesn’t exist. That makes this idea look less like an adjustment and more like an outright import tariff. In discussing this whole border adjustment concept with other economists, I find general agreement that my description of the BAT as a “half-assed VAT” is generally correct. That is perhaps not a politically correct way to state the matter in a letter that may be read by the faint of heart, but it does paint an accurate picture that will save you a lot of reading time, so I’ve just gone ahead and put it that way. Free, or Fair? Here I need to stop and explain something. I believe that truly free trade helps everyone, but that’s not what recent so-called free trade deals have given us. Instead, they delivered something quite different from the kind of free trade that Adam Smith and David Ricardo envisioned. I explained this at length last July in “The Trouble with Trade.” Here’s an excerpt: “Free trade” deals are no longer simple documents. The Trans-Pacific Partnership (TPP) weighs in at 5,544 pages. It’s a boatload of rules and regulations. I know there is talk that this deal was negotiated in secret, but that is far from the truth. You and I weren’t asked for input; but lots of people were, let me assure you. I can guarantee you that rice farmers in Texas and California were pressing their congressmen and others for access to the lucrative Japanese market, and Japanese rice farmers were trying to figure out how to limit the damage. For the record, Japan imports about 10% of its rice from the US, most of which they turn around and export as foreign aid or use for animal food. It is not that Japanese rice is that much better; indeed, the fact that US rice is so close in quality makes Japanese farmers nervous. And US rice is 1/3 to 1/2 the cost of Japanese rice. Of course Japanese companies want access to US markets, where they can compete quite well, thank you, against US firms. And those US firms want to keep the protections and prices they have. This tit for tat has gone back and forth in hundreds of industries in the 12 countries involved in the TPP. I can guarantee you that wheat farmers or corn farmers or cattle or hog producers have a different view of the whole process than US rice farmers do. And their views are different again from those of equipment manufacturers or software developers, or pick any of 1,000 industries. Rice farmers in Japan have to negotiate terms of trade with other national industries, and do you think New Zealand avocado farms or sheep farmers or movie firms have any less interest in the process? Every country is worried about US companies coming in and overwhelming their businesses, and the US is worried about “unfair” competition – that is, competitors in other countries producing products that are cheaper or better. Often, the higher cost of products here is attributable to the regulations that we impose on our own industries. So we want other countries to abide by our regulations (and they want us to abide by theirs). The problem with global deals like TPP and its US-European counterpart, TTIP, is that while they may be good for the economies as a whole, citizens will find that “good” very unevenly distributed, which is why Trump calls such agreements “a job and independence threat.” After supporting the TPP for several years, Clinton now says she will not sign. Both candidates are responding to the very real problems generated by the uneven distribution of globalization’s benefits over the last 30 years [emphasis mine]. Read that last paragraph again, because it’s critical. In fact, it’s the core problem behind most of our current ills. Global trade grew enormously in recent decades, but its benefits were distributed in ways that left many people out. I have used the following line from William Gibson over and over again, but I do so because it is the single best description of our world today: “The future is already here; it’s just unevenly distributed.” The benefits of technological advancement and economic globalization have been unevenly distributed. See, for reference, the Rust Belt of the US. Note that this is why a Donald Trump was elected. He recognized and addressed the suffering before other presidential candidates did and capitalized on it. Good on him as an observer of our times. For a variety of social, political, and economic reasons, we can’t let this uneven distribution continue. A significant number of our fellow citizens are demanding change. But the uneven distribution will continue if the US enacts this border adjustment tax plan. It should be clear to everyone that Brexit and Trump and all the other nationalist movements are not happening in a vacuum. Trump is not the final expression but the harbinger of a swelling trend that will be felt throughout the world. Those who are left out of participating in future economic abundance are going to be pushing back; and while this time the Republicans were able to take advantage of the situation, the next time it will be the Democrats or some other group that does so if the Republicans don’t figure it out. If we don’t learn how to more evenly distribute the benefits of accelerating technological changes and globalization, we are going to see ever more pushback, not less. And the next time it will not be the Democrats who are worried about the end of the world, but the Republicans. I just want to say that it is really, really, really, really important that we get it right this time. The cost of screwing this up will be far greater than you can possibly imagine. Conservatives may not have another shot for a very long time. Think Herbert Hoover. (See more below.) Tariffs Ruin Christmas Under the BAT plan, imports will be penalized and exports rewarded, which, theoretically, in a perfect world without pushback, would leave our economy nicely balanced and undisrupted. That’s the idea. But I doubt it will happen that way, because the importers and exporters are not the same businesses. A vast number of businesses import products from other countries and sell them to Americans. Toy companies are a good example. Virtually all the shiny presents under your Christmas tree were made outside the US. The companies that import them could be border-adjusted right out of business under the Better Way plan. Here’s an example. Suppose you are a toy company and you spend $1 million to bring in toys from China. You package and distribute them to retailers around the country, generating an additional $500,000 in costs for yourself. You sell them at wholesale for $2 million. What’s the tax consequence? You just spent $1.5 million to generate $2 million in revenue. But the $1 million you spent on the imports is no longer deductible on your tax return. So your taxable profit isn’t $500,000, it’s $1.5 million. At 20%, your corporate income tax is $300,000 instead of $100,000. This plan triples your taxes. Would you stay in business under this plan? Maybe, but you would certainly raise your prices. Would the retailers and consumers still buy as many toys? Probably not. You will have to downsize and probably lay off workers. That’s not good for anyone. What the Republicans want us to do is to buy American-made toys instead of Chinese imports. Does that manufacturing capacity exist in the US, with the same net prices and quality you get from the Chinese suppliers? Probably not, or we would already be using it. It will emerge if the demand exists, but not instantly. And, with the BAT in place, US-manufactured products that compete with the products we buy from foreign producers will cost 20% more, priced in US dollars. Meanwhile, those who export products from the US will see the reverse effect. Their tax bills will be slashed since their foreign revenue will no longer count as taxable revenue. They’ll probably expand and hire more workers. So maybe it will work out. Exporters will hire the laid-off import workers. Maybe – if the skills they possess are the same as those that were just rendered unnecessary at the importers’ operations, and if automation doesn’t cost less than paying humans. At best there will be an adjustment period, which will be far longer than those who propose this plan think, as workers retrain for new jobs. We’ve heard this story before, and it didn’t work out as advertised. So count me skeptical. The problem is that the importers and exporters don’t all operate in the same states and counties, so the people who lose their jobs because of the import tax will end up having to move to where the exporting jobs are. How did that work out for the Rust Belt when the steel jobs left? For whatever reason, the data clearly shows we are moving less than we ever have before. But that’s a topic for another letter. Retail Rubble As you might expect, the retailing industry is dead set against the BAT. Walmart, Target, and the like are already lobbying hard against it. One of the experts I spoke with, when I asked about retailer opposition, let out a big sigh and said the National Retail Federation has always been against any kind of consumption tax. As I thought about that later, it made sense. “Consumption” is what retailers sell. They want us all to consume more stuff from their stores. Consumption taxes reduce the amount their customers have available to spend, so these taxes are a direct revenue loss to retailers, at least in the short term – and the short term is 5 to 10 years. These types of adjustments do not come quickly. The retailers aren’t just whistling Dixie. The BAT would hit them hard at a time when they can’t afford many more hits. The 2016 holiday season was a blazing success for Amazon and its online brethren (including Walmart, which now has a large online presence). For everyone else, not so much. E-commerce finally seems to have reached critical mass. It is now proceeding to vaporize the competition. Retailing at scale is all about logistics. You need to get the right products in front of the right consumers at the right time, and not a minute sooner or later. The big box stores actually do a pretty good job of that, but now they have a new problem. Consumers carry these little comparison-shopping supercomputers (courtesy of Apple, Samsung and others – and by the way, these are imported products and would cost 20% more, post-BAT) in their pockets and are not shy about finding a better price. Amazon usually has what you want for less if you are willing to wait a day or two. Worse, Amazon is compressing that time. They have built a stunning network of highly automated warehouses around major cities. They’re in the process of building a drone air force to further speed deliveries. Here in Dallas you can get same-day delivery of many items, at the same or better prices than brick and mortar retailers charge. A few clicks and it’s on its way; you don’t have to drive to the store only to discover it doesn’t have the brand that got the best reviews. The Amazon business model is working better in today’s economy. That’s just a fact. Now, Amazon sells many imported products. So does Walmart. The border adjustment will hit both of them, but it will hit the old-style retailers just as hard, at the very time they are struggling to compete with Amazon. Walmart may survive. I’m not sure companies like Sears will. I’m very frustrated with some of my Republican friends who don’t see this, or who blithely assume new jobs will magically appear for those displaced. We have seen in the present “recovery” that this is no longer true. This is a time of wrenching change. We have to find better ways to help people adjust to these changes. Yes, the market will provide new opportunities, but human beings are not identical bricks that you can just rearrange in new piles. In conversations with border adjustment proponents, I’ve heard very little about implementation plans. They don’t seem to have considered how to get the economy and the population from here to there in a way that avoids negative transition costs. That’s a big problem. Even if it all works according to plan, there will be pain in the transition. This is like the weather bureau’s cheerily telling us it will be sunny and warm day after tomorrow, right after the category 5 hurricane passes through. They are getting a little ahead of themselves. Understand, I wouldn’t be so against the BAT if we could fast-forward five years and arrive at the new equilibrium point without all the adjustments that will have to happen in the meantime. These adjustments are going to be more problematic than you can imagine. Manufacturing Jobs Are the Last War As I mentioned in part one, 80% of the manufacturing jobs that have gone away in the past 20 years have been displaced by technology, not “offshoring.” That trend is not going to stop anytime soon, and those jobs are not coming back. Please note that we are now manufacturing more than we ever have, just with dramatically fewer people. Also note: Some of the people in the Trump administration are critical of Germany and their export-heavy model. I agree that Germany is a problem. But let me point out that in the next global recession (and there’s always a next global recession) a country that depends on exports for 50% of its GDP is going to get its throat ripped out. Especially when the euro breaks up and nobody has the ability to buy Germany’s high-priced products. There is a cost that comes with being a manufacturing power, and you need to be careful what you wish for. The manufacturing fetish that some Republicans are gripped by comes with a price tag. And note that some of the products we think of as “US-manufactured” have significant components made all over the world. I could literally offer you 100 major examples, but consider the Boeing 787. Boeing sales are a big part of our dollar exports and technological prowess. How much more American could you get than Boeing? Well, a lot more than you might think.  But that eye-opening reality still misses a most important point: Manufacturing jobs are truly the last war. The next front in the “jobs war” is going to be the service economy. When (I consider when more likely than if) Sears goes under, that is 178,000 mostly service jobs that will be gone. Saving a few manufacturing jobs here and there is nice, but it doesn’t balance out losing 178,000 service jobs. Starting in about five years, automated driving will put truck drivers and taxi drivers out of work. Where will those 3 million workers find jobs? There are hundreds of small stores and establishments in the service industry that are going to be “disintermediated” out of business, which is a fancy way of saying that online and more efficient establishments will be taking or eliminating their jobs. There are literally going to be millions of service jobs at risk in the near future if we don’t come up with some way of creating new industries from whole cloth. (That challenge will be the subject of a number of future letters. It’s critical to the future of every country in the world.) That is why I applaud the idea of what the Republicans are trying to do with the Better Way plan, because they are trying to stimulate new businesses in the United States. New businesses are the font from which growth and new jobs spring. However, the mechanism by which they plan to accomplish this laudable goal is going to create more problems than it solves. Dollar Disaster In their defense, Paul Ryan and House Ways & Means Committee Chair Kevin Brady know everything I just said and probably agree with much of it. They believe the BAT’s negative effects will disappear quickly due to currency flows. As the trade deficit shrinks, fewer dollars will flow from the US to the rest of the world. That trend will make the dollar rise against other currencies, thereby nullifying the higher prices we will pay for imported goods. That’s the theory. In fact, most economists do agree that the dollar is likely to rise significantly if this proposal is adopted. So, the theory is that Walmart shoppers really won’t pay higher prices, at least in dollar terms. I do not think things will work that way in practice, at least not as quickly as they hope. My Camp Kotok friend Megan Greene, who is the chief economist at Manulife Asset Management, explained why in a Financial Times column earlier this month (emphasis mine): The US dollar will take years to adjust. There has historically been about a five-year lag between a current account shock and a full adjustment in the real effective exchange rate. Prices tend to be sticky [This is a critical point! Pay attention! – JM], particularly when 93 per cent of US imports and more than 40 per cent of global trade is invoiced in US dollars. These prices would have to be renegotiated over time. Furthermore, the Federal Reserve and the People’s Bank of China would do their best to lean against such a currency move. In the short to medium term, importers would pass the cost of the border tax on to US consumers, who have been driving the economic recovery. Hitting them could significantly undermine growth at a time when inflation is accelerating, resulting in stagflation. Eventually, the dollar will appreciate. But the impact of the tax may then be even more grim because of the US dollar’s role as the global reserve currency. Nearly $10tn of outstanding offshore debt is denominated in dollars. According to the Bank for International Settlements, about 90 per cent of Turkey’s sovereign debt and more than 80 per cent of China and South Korea’s non-financial corporate debt is dollar-denominated. A 15–25 per cent appreciation of the dollar would make this debt much harder to service and would tighten financial conditions in these countries and across emerging markets. Here we see once again how debt constrains us from doing what might otherwise make sense. Emerging-market countries own massive amounts of dollar-denominated debt. A stronger dollar means they must somehow come up with more of their local currencies to repay their dollar debts. And they will have to do it fast, even as their exports are shrinking because US consumers are being encouraged to “buy American.” It gets worse. To whom is all that emerging-market debt owed? Primarily to Western banks and bondholders, who are often themselves excessively indebted. The potential financial contagion is massive. Ambrose Evans-Pritchard of the London Telegraph describes it in his characteristically colorful style: Yet getting there constitutes a global shock of the first order. “This will trigger a series of emerging market crises,” said Stan Veuger from the American Enterprise Institute. He estimates that the burden for companies and states in developing countries with dollars debts will jump by $750bn. Turkish firms alone would face a $60bn hit. It does not end there. Studies by the Bank for International Settlements show that a rising dollar automatically forces banks in Europe and the Far East to shrink cross-border lending through the mechanism of hedge contracts. A dollar spike of anywhere near 20pc would send the Chinese yuan smashing through multiple lines of psychological resistance. The People’s Bank (PBOC) is already intervening heavily to defend the line of seven yuan to the dollar. Ferocious curbs would be needed to stop the Chinese middle classes funneling money out of the country if it crashed by a fifth. Junheng Li from Warren Capital says the China’s exchange regime is more brittle than it looks. Official data overstates the PBOC’s fighting fund by $1 trillion, either because reserves are “encumbered” by forward dollar sales or because they must be held in reserve as a “fiscal backstop” for Chinese firms at risk of default on dollar debts. She expects the system to snap at any time, and without warning. I strongly doubt whether the Trump-Ryan axis in Washington has any idea what could happen if they detonate a debt-deflation crisis in China, or if they ignite a short-squeeze on $10 trillion of off-shore dollar debt with no lender-of-last-resort behind it. Nor do they care. I disagree with that last part. I think Trump and Ryan certainly do care about setting off a global crisis. They just don’t think they will. And this is where I think they are ignoring basic game theory. The world economy is currently ensconced in the equivalent of a Nash equilibrium. What that means is that everybody has adjusted to the present rules by which the dollar is the world’s reserve currency; the US agrees to run large trade deficits, flowing dollars to the rest of the world so that the USD can remain the reserve currency; and global trade is based largely around current global tax policies remaining largely stable. Game Theory: Destroying the Nash Equilibrium When you talk to Republican leaders and ask them why other countries wouldn’t react to the BAT and impose larger tariffs or sanctions on US goods, they respond with a question of their own; and it’s a logical one: “But why would they? We’re only doing with the BAT what they’re already doing to us.” And they are correct. US corporations are at a massive competitive disadvantage today because we have high corporate taxes and no VAT. Other nations do not charge a VAT tax when their companies export products. That means a German car sold in Asia or a Japanese car sold in Europe has a competitive tax advantage over a car made in the US and on sale in those countries. The Republicans are simply trying to rectify that competitive disadvantage. The problem is that other countries are simply not going to say, “Oh, the United States finally figured it out that we were taking advantage of its silly, complicated tax system. There’s really nothing we can do, so let’s just get on with the program.” No, they are going to protect their own businesses. In international trade, it’s every country for itself. They are all going to react to losing anything that they think is a competitive advantage. If you don’t get this, go back to kindergarten and study children trading toys in their sandbox. This behavior is ingrained in every human being. Game theory clearly demonstrates that when one player interrupts the Nash equilibrium, the other players will respond; and the responses will go back and forth, tit for tat, until there is a new equilibrium. The question is, what will be the process that the world has to go through in order to find that new equilibrium, and do we really want to see that process play out? We are going to revisit that process in just a bit, but first I want to go back and show you again a few paragraphs from Charles Gave’s piece that I quoted extensively in part one of this series. You really should go back and read it in full if you haven’t. (Emphasis mine.) I exaggerate for effect, but this example shows that the US’s “exorbitant privilege” [because ours is still the world’s reserve currency –JM] has little to do with free market principles as it means the US (i) lacks a foreign trade constraint, and (ii) can force other countries to accept payment in dollars. Should either of these conditions end then the credit pyramid would implode. And indeed for decades commentators have fretted that the rest of the world may one day lose confidence in the US dollar as a store of value, resulting in soaring US interest rates and an economic crash – the Japanese, Chinese and a Brazilian supermodel have, at different times, all been touted as potential liquidators. I never believed such scare stories so long as the US remained a superpower capable of corralling international respect. What worried me was a situation where the US, for domestic political reasons, pulled up the drawbridge and chose to pursue a current account surplus. Such an outcome was always going to be driven by Americans at large concluding that the global production system was being run against their interests. [This is the critical understanding that you must grasp! – JM] Revisiting Hooverville While I don’t think (please God) we are anywhere close to implementing a policy as draconian as Herbert Hoover’s was in the late 1920s, it would behoove us to remember his Mexican Repatriation, by which somewhere between 500,000 and 2 million American residents of Mexican ancestry were forcibly returned to Mexico. Many of these deportees were actually US citizens. And this was done without due process. I kid you not. By the way, this program was continued by Franklin D. Roosevelt for another four years. This program is a dark blot on American history, one that I think was even worse than the Japanese internment camps of World War II. The expulsion was carried out in the name of “protecting American jobs” and putting America first; and then it was followed up with policies that were designed to make America productive again, including the Smoot-Hawley Tariff Act, which was a contributing factor in the Great Depression. I have written for over 17 years – since I first started to pen this letter, that the single thing that scares me more than any other potential economic event is a move toward protectionism and a resulting global trade and currency war. There is simply no other force that would be more destructive to your personal wealth and lifestyle than this.  The situation of the late ’20s and early ’30s is precisely the one that Charles was referring to: America decided that the global production playing field was tilted against American interests and needed to be leveled. I don’t think anybody today would want to go back to the 1930s. Nobody wants another Great Depression. Again, let me remind you that FDR did not repeal Smoot-Hawley and continued many of Hoover’s destructive policies . There is plenty of bipartisan blame and shame to go around here. A Most Intricately Balanced Nash Equilibrium The global economy is orders of magnitude more intertwined than it was in the 1920s and ’30s. Let me list a few of its challenges for you, things that we have touched on in previous letters and a few new ones: 1. The developed countries are awash in debt that totals around $150 trillion. 2. As mentioned above, emerging-market countries have $10 trillion of US dollar-denominated debt that they would be unable to pay back if the dollar were to rise by 20%. We would experience a global banking crisis whose proportions would dwarf anything we’ve seen to date. Think subprime debt on steroids. 3. It is going to take at least a trillion euros to solve the Italian banking crisis, which is an amount of money that the Italians simply do not have. The only way they can get it is for the European Central Bank to buy the bonds that the Bank of Italy would have to issue. That means Germany would have to blink and participate in the financing of that debt. That rescue would raise Italy’s debt-to-GDP ratio well north of 175%. Think Greece writ large. How in the wide, wide world of central banks and monetization do you think the Italians, whose economy is growing at barely 1%, can ever repay that debt? Seriously? You think I’m exaggerating about €1 trillion? Do the math and then factor in that the NPLs on the Italian balance sheets will be double or triple the current stated size in a crisis. I was told I was crazy when I said in 2006 that we would lose $400 billion to the subprime crisis. That was about the time when Fed Chair Bernanke was telling us the subprime crisis could be contained. I was an optimist by at least a trillion dollars, give or take. Looking ahead, €1 trillion may be a similarly overoptimistic estimate of what it will take to resolve the Italian banking crisis. 4. Brexit? Do you really think the Brexit negotiations are going to be a walk in a park, given the nationalist tendencies that are emerging in Europe? 5. Japan is continuing to massively monetize its debt. The Japanese have no choice. Their currency is going to continue to fall. I know that Abe and Trump were playing nice last week, but when the yen hits 140 or 150 because the dollar is rising and you can buy a Lexus cheaper than you can buy a Hyundai, how does that work for the trade protectionists in the Trump administration? 6. President Trump has expressed concern about certain currencies being manipulated and thus being too weak. A crisis in Europe and Britain would result in their currencies dropping, along with the yen, forcing China to allow its currency to drift downward, too, since China is exposed to all of those countries through its own trade. China simply does not have enough dollars to support its currency at the current level if the dollar were to rise by 20%. To try to do so would destroy their balance sheet. But to allow the yuan to fall would sabotage their current push toward becoming a consumer society and would create an enormous amount of instability. They would be forced to double down on their mercantilist strategy. In other words, an escalating trade war! 7. One thing that nearly all economists agree on is that if we pass the border adjustment tax as currently proposed, the dollar would (eventually if not quickly) rise by about 20%. In fact, the Republicans actually use that as a selling point to show that the BAT wouldn’t really increase the cost of our imports, never mind the fact that our imports are priced in dollars and not in foreign currencies. (Remember Megan’s point about “price stickiness” above.) To say that the transition would be messy is an understatement. 8. Global market valuations of all asset classes are about as high as they have been in a long time. When was the last time we had interest rates so low and equity market valuations so high? Does this seem like a bubble do you? Or at least the beginning conditions for one? 9. If the dollar does rise too much, does President Trump instruct the Department of the Treasury to monetize our debt in order to weaken our own currency in response? Isn’t that called a currency war? 10. If our currency rises, the advantage that our exporters get from having to pay no income tax on their exports disappears at the border. Okay, you get the picture. The world is in a pretty $#&^% fragile place right now, and you want to be very careful if you aim to upset and reset the Nash equilibrium. Understand, I am not arguing that we don’t need to change things. We just need to be $&%%&* (multiple expletives deleted) careful about how we go about it. I know this is going to offend a few of my friends, but I’m going to say it anyway: I am afraid that this border adjustment tax, if implemented, will throw the world into a global recession. All of the wonderful tax cuts and beautiful plans that are being proposed along with the BAT will not be enough to keep the US from participating in that recession as well. Understand, I’m a believer in free markets, and I know that the American enterprise and entrepreneurial system, when given an opportunity, can respond and create growth in this country. But the BAT is not the way to do it. More on how to do it later in next week’s letter. Striking Out at the WTO The Republican plan has another problem, too. It likely violates World Trade Organization rules. The European Union is already preparing its challenge. President Trump has talked of possibly leaving the WTO, which might not be all that bad a move, though it would set off a complete reworking of how global trade is done. That process could spin out of control quickly. And remember, while the US may be the largest player, we’re only 25% of the global economy. The rest of the world might just say, let’s see what we can do without the US and go ahead and create our own reserve currency so that we don’t have to depend on the US’s injecting massive amounts of dollars into global markets. America may be first, but there are a lot of other countries that think they are second or third, and they have nationalist movements of their own. The proponents of the BAT argue that it is technically within the rules of the WTO. I am neither a global trade lawyer nor the son of a global trade lawyer, and I don’t know the technicalities of those rules. But I am pretty good country boy observer of the political process. The WTO is not like the US Supreme Court, which is bound to operate according to the US Constitution. The WTO is a political process. Call me skeptical, but I don’t think President Trump has a lot of political capital to spend at the WTO. I think the likelihood that he would lose a WTO ruling is damn near certain. If he does, we can either try to change the rules or leave the WTO. The volatility that would surround the US’s departure from the WTO would be quite impressive. Global markets would absolutely collapse, and the Trump bull market would quickly morph into the Trump bear market. Think Hoover. Which is one reason I don’t think Trump will actually support the BAT. Fingers crossed. The broader point is that all this potential turmoil is avoidable. There is a much better way that Trump and Ryan and the Republican team, in cooperation with the Democrats, can simplify the tax code without risking trade chaos, a global recession and possibly a global depression. We can achieve everything we are trying to do, give US entrepreneurs and businesses the impetus and capital they need to launch one new business after another, create the jobs that we so desperately need, and simplify the tax system while balancing the budget. And we can give every worker in the United States a significant pay raise without even touching the concept of increasing the minimum wage. Sound like pie in the sky? No, but it means real change … which will require real change. Understand, there are winners and losers in every serious tax change, including in my proposal. And my proposal will mess with the Nash equilibrium, but it will do so in a less abrupt manner and allow for a transition to a smoother and new equilibrium without instigating a trade war. US businesses will still get their border advantage, and we can actually find the capital for literally hundreds of thousands of new businesses that will create millions of jobs. You can say that I’m a dreamer, but I’m not the only one. New Jersey and the Gym I know I’m going to be making a number of impromptu one-day trips, but the next one that’s planned will have me in New Jersey, where I’ll be speaking on March 14 and 15 to potential individual investors about our new Mauldin Smart Core Portfolios strategy at a seminar with Steve Blumenthal of CMG and The Financial Quarterback’s Josh Jalinski of WOR and WABC in the New York City metropolitan area and New Jersey. You must reserve a spot with Josh’s office at 888-988-5674(JOSH). I finish this letter at the brand-new Kimpton Seafire Resort in the Cayman Islands. I’m at one of my favorite conferences of the year, the Cayman Alternative Investment Summit, which is normally held at the Ritz here on the island. I was a little concerned about its moving from the Ritz, but the Kimpton is actually quite the superior hotel. If you’re looking for a vacation in the Caymans, you should consider it. This has been an extremely interesting conference. The attendees are generally institutional and family office investors, and the conversations this year were remarkably candid. There is a concern about how long the current status quo can continue and what these institutions, which generally have mandates that limit their flexibility, can actually do to protect themselves from what everybody tends to agree will eventually be a crisis. I listened to a number of the presentations, and what I heard is forcing me to think through some new alternatives for how we can hit the global reset button on too much debt and handle the popping of the bubble of government promises. We are truly going to have to learn to think the unthinkable. When we come to the next crisis, we will be forced choose the least painful path, a choice that might normally have us run screaming for the exits. But that may be what we have to do. More on that happy topic in later letters. We actually had Arnold Schwarzenegger here yesterday. He gave a most encouraging and uplifting speech. At the end of his talk I was allowed to ask a question. I wanted to know what it was like to come to the United States, go to “Muscle Beach” in Venice, and work out in Gold’s Gym, otherwise known as the Dungeon, with the likes of Dave Draper and all the other weightlifting heroes. That was not a question I think he was expecting, and he thought about it for a second, then began to describe the weightlifting and bodybuilding scene of that era (the late ’60s and early ’70s). Not only bodybuilders but power lifters and Olympic weightlifters all trained in this one small gym. They all pushed each other to outperform. Literally, he would work out with three to four former Mr. Universes, Olympic gold medalists, and multiple other champions in a variety of competitive sports. It was truly something that will never happen again, because you will never see that concentration of highly competitive people in one small space, with only the most rudimentary of gym equipment at the very dawn of an industry. Now every hotel you go into has a gym. Hospitals routinely put you into resistance training in your rehab. These guys changed the way we think about growing old and maintaining our bodies. By the way, let me give a shout out to my friend Dave Draper, known as the Blonde Bomber, who was the Mr. Universe right before Arnold began his amazing run of championships. Dave simply has the best protein powder I have ever tried, and if you are looking for something that actually tastes good to help control your weight, I recommend what he calls his Bomber Blend. It is the best combination of nutrients and protein that I’ve ever been able to find. You can get it at davedraper.com/fitness_products/product/QPD-SBB.html. You should also consider subscribing to his free weekly letter, which is part of my motivational routine to keep me in the gym. Iron and steel are your friends. (Read Dave&rs quo;s book, Brother Iron, Sister Steel.) Last night Shane and I had tickets for the legends tennis match, where we watched 58-year-old John McEnroe, 48-year-old Jim Courier, and 62-year-old Chris Evert run around on the court with their competitive genes still obviously alive and kicking, even if their serves and returns did not have their former zing. And they were having fun with the crowd and each other. They played legends music between games – Queen, AC/DC, Bon Jovi, Kiss, the Eagles, etc. After McEnroe dispatched Courier, he celebrated by dancing with the young kids. It was a hoot. Between the tennis greats and 71-year-old Arnold, they just make me want to work out more and stay in shape. Or maybe get in shape. And with that, I will hit the send button, momentarily ignore my inspirations, and go sit on the beach for an afternoon and read and maybe relax before heading back to a full workload in Dallas. You have a great week! Your fighting the good fight against aging too fast analyst,

John Mauldin

subscribers@MauldinEconomics.com Copyright 2017 John Mauldin. All Rights Reserved. | Get a Bird’s-Eye View of the Economy with

John Mauldin’s Thoughts from the Frontline

This wildly popular newsletter by celebrated economic commentator, John Mauldin, is a must-read for informed investors who want to go beyond the mainstream media hype and find out about the trends and traps to watch out for. Join hundreds of thousands of fans worldwide, as John uncovers macroeconomic truths in Thoughts from the Frontline. Get it free in your inbox every Monday. |

Share Your Thoughts on This Article

http://www.mauldineconomics.com/members Thoughts From the Frontline is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com. Any full reproduction of Thoughts from the Frontline is prohibited without express written permission. If you would like to quote brief portions only, please reference www.MauldinEconomics.com, keep all links within the portion being used fully active and intact, and include a link to www.mauldineconomics.com/important-disclosures. You can contact affiliates@mauldineconomics.com for more information about our content use policy. http://www.mauldineconomics.com/subscribe Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President of Mauldin Solutions, LLC which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA and SIPC, through which securities may be offered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Mille nnium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee. Note: Joining the Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Mauldin Solutions, LLC, which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millenni um Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements. PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account manager s have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273. |