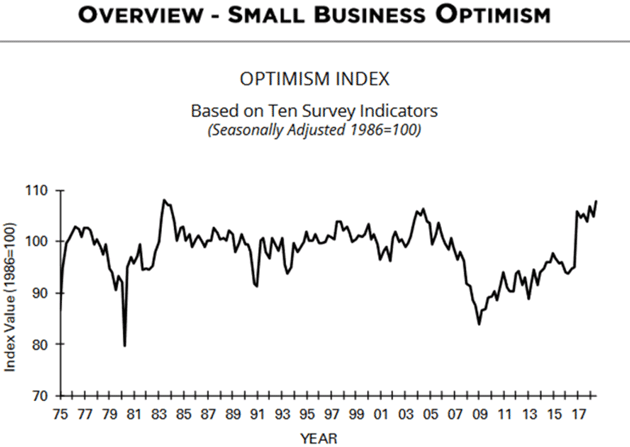

The Good News Economy By John Mauldin | Aug 18, 2018 In my business, there is a fine line between standing by your conclusions and being unwisely stubborn. But no matter what I say, people will still label me a perma-bear or perma-bull—often at the same time. It’s an occupational hazard to which I am accustomed. It’s really a lot more fair to characterize me as the “Muddle Through” guy. There are always reasons to be bullish or bearish. Admittedly, my letter tends to dwell more on the reasons to worry, but I think that’s a sign of the times. We have more to worry about today than in the past (see the 80s and 90s). Last week, I tried to clarify what some of you perceive as inconsistencies in my outlook. I am long-term very bullish, medium-term very bearish, and short-term uncertain to slightly negative. If you read social media or the mainstream financial news, you don’t need me to tell you the bearish case. Skepticism abounds in the punditry. Positive outlooks are harder to find, even though they have been largely correct recently. That’s no accident. They’re correct in part because they are out of favor. I see some major problems coming in the 2020s (and perhaps a bit sooner), but I also see a lot of good things happening right now. The economic recovery, while still weak by historic standards, is gaining some momentum that ought to carry it forward for another year or two, assuming (as I perhaps naïvely do) that we can put this trade war thing to rest. That’s good news because it buys us time to prepare for worse times, but it’s also just plain good news. We can get so busy worrying about the future that we ignore positive things happening right here and now. That’s not healthy and can make us overlook opportunities. So today, I’ll look at some good economic news that has been lost in the din lately. Economic activity is the collective result of human decisions. We all make choices about what to buy and sell and at what prices we will do so, thereby creating either growth or contraction. These decisions might prove wrong, but they still matter. So do the attitudes and beliefs that lead us to make them. If, for instance, you’re a business owner and you see new conditions that will make growth easier, you will be more likely to hire, expand, and make capital investments. Get enough businesses thinking that way at the same time and you have the makings of an economic boom… which is what the leading survey of small business owners says is happening. The National Federation of Independent Business has been surveying its small business members since 1973, overseen by my very good friend Dr. Bill Dunkelberg (Dunk to his friends). The NFIB data is a rich, long-term history of small business owner sentiment, both positive and negative. It has varied over time, as you might expect. Presently, their index is near its most optimistic level ever—0.1% below the 1983 all-time high. Considering where we were a few years ago, that is amazing.

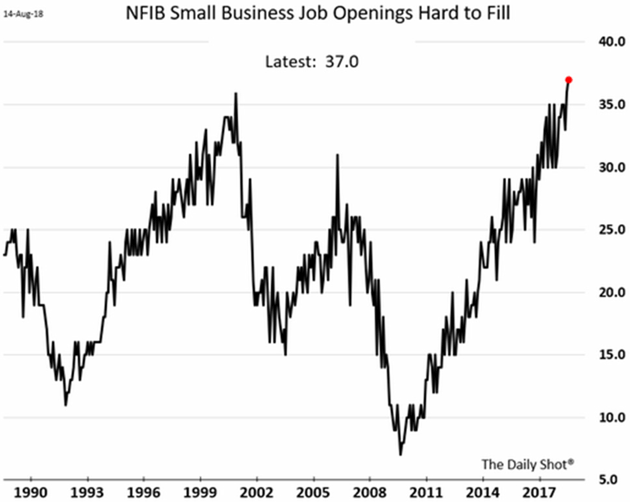

Source: NFIB As you can see, NFIB member optimism had two prior peaks near the current level. One was in 2004, when the housing boom was starting to take off. It would end badly a few years later, but those were good times while they lasted. The other peak was in 1983. The Volcker Fed had mostly stamped out inflation while Reagan’s tax cuts and deregulation were beginning to bear fruit. This marked a boom period that would last even longer; the next recession would not strike until mid-1990. As I like to say, history doesn’t repeat itself, but it often rhymes. This time, the Fed has been working to stamp out deflation, not inflation, and appears to have made some progress. We also have a new, business-oriented administration, similar in some respects to the shift from Carter to Reagan. This encouraged early 1980s business owners, and the Trump administration is doing the same now. See that big late-2016 leap in the NFIB index? That happened immediately after the election. If you recall, almost everyone expected a Hillary Clinton win, and business owners had resigned themselves to continued high taxes and evermore intrusive regulation. The Trump win was thus a pleasant surprise to many business owners, immediately visible in the data. (Contrary to some, I don’t think most business owners were thrilled with Trump. They were more thrilled not to have Clinton.) Now, why does this matter? It matters because NFIB members create jobs, spend money on capital investments that create even more jobs, and develop innovative products that raise living standards. They are more likely to do all those things when they feel confident... which they have since November 2016. Notably, this confidence has actually grown since then despite all the assorted scandals and criticism surrounding the Trump administration, not to mention the Federal Reserve’s tightening policy. This would not have persisted for almost two years now if they didn’t see reasons for optimism in their own numbers. It is more than blind faith. In the past, we’ve seen this index decline gradually over 2–3 years as the economy edged toward recession. We see no such thing now. We see the opposite as the index moves up. That suggests, as I heard at Camp Kotok, the present expansion will continue into 2019 and beyond. Could something change the small business outlook? Yes, of course, but no such event is on the radar right now. One of the NFIB indicators is the difficulty small business owners have in filling job positions. Right now, it’s at a record high, with many owners reporting qualified worker shortages as their single greatest business challenge.

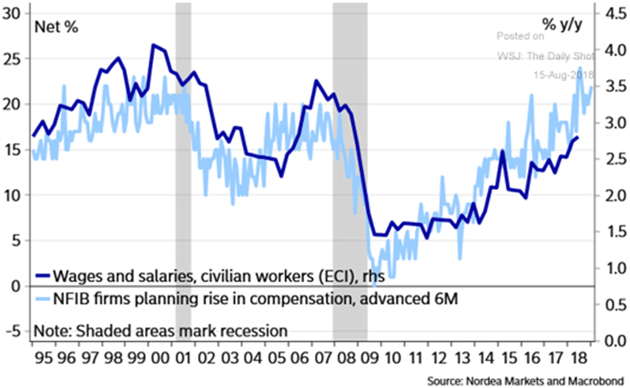

Source: Daily Shot This is a consequence of another “good news” item: historically low unemployment. It took way too long after the last recession, but employers are finally willing to expand payrolls. They can do so only because they expect sales to grow beyond their present capacity to deliver, which is why business sentiment is so important. Moreover, the hardest-to-employ groups (unskilled workers, people with criminal records, those with disabilities) are finally re-entering the labor force. Workers see opportunity to make more money than they can from government benefits or whatever other means of support that have relied on. Who gets credit for this? It’s true that the job gains simply continue trends begun under the Obama administration. Whether Obama policies did it is a different question. The economy was recovering regardless. Trump could certainly have done things to interrupt the recovery, so give him credit for not doing them. And the business confidence he inspired by being “not Hillary Clinton” helped, too. My friend—and sometimes debate opponent—Brian Wesbury, who is chief economist at First Trust, has been consistently right about the employment trends in recent years while many of us were skeptical. I’m starting to pay more attention to his outlook. Here is Wesbury’s analysis of the July jobs report, with some key points bolded by me. The July employment report was sneaky strong. The big headline was that non-farm payrolls rose 157,000 in July, which was less than the forecast of any economics group. However, payroll growth was revised up 59,000 for May and June, meaning the net gain for the July report was 216,000, which beat the consensus expected gain of 193,000. Meanwhile, civilian employment, an alternative measure of jobs that includes small-business start-ups, rose 389,000. In the past year, non-farm payrolls are up 200,000 per month while civilian employment is up 179,000 per month, both strong numbers. The gain in civilian employment in July helped push the unemployment rate down to 3.9%, despite an increase in the labor force, which is up 1.5 million in the past year. Moreover, the U-6 unemployment rate, which includes discouraged and marginally-attached workers, as well as those working part-time who say they want full-time jobs, fell to 7.5%, the lowest level since 2001. The participation rate remained at 62.9% in July, near the higher end of its past 4+ year range (62.3% and 63.1%). Meanwhile, the share of the age 16+ population that's working hit 60.5%, the highest since 2009. As always, we like to measure growth in workers' total cash earnings. Average hourly earnings rose 0.3% in July and are up 2.7% in the past year. Total hours worked are up 2.2% in the past year. As a result, total cash earnings—which exclude extra earnings from irregular bonuses and commissions, like those paid out after the tax cut was passed—are up 5.0% in the past year, more than enough to keep pushing consumer spending higher. We see this in another chart from the NFIB data, showing small businesses’ plans to increase compensation. The expectations line is moved forward six months, showing where the trend is going.

Source: Daily Shot We also see record numbers quitting their jobs, which is actually quite bullish. You generally only leave a job if you get a better one or at least think one is out there. As Brian said, wages are beginning to grow, too. That is the last piece of the puzzle. We need people to have more disposable income so they can buy the goods and services businesses produce. It finally seems to be happening. And the simple fact of the matter is that sometimes you have to pay people more in order to attract them. I have been a small businessman for about 45 years and lived through several cycles. Right now, every business owner I’m talking to says they’re having to pay higher wages. Earlier this summer, my associate Patrick Watson wrote about Overheated Highways clogged with trucks. I see the same in private transportation newsletters I get. US railroads and seaports are bustling, to the point that shipping costs and logistical snarls are now major challenges for many businesses. That’s not great… but it’s also not consistent with economic slowdown forecasts. To be blunt, businesses are spending enormous amounts of money to transport enormous quantities of raw materials and finished goods across the country. They are not doing it for fun, or because they enjoy paying truck drivers relatively high wages. They believe someone will buy those goods at profitable prices despite the transport cost. Maybe they’re wrong, but that is what they think. Patrick pointed out in his article, “Slow and unpredictable shipping has a domino effect in our optimized, just-in-time economy. One key part that’s stuck in a traffic jam can shut down an entire assembly line, idling hundreds of workers. Then whoever is expecting those goods doesn’t get them on time.” This is indeed happening. Last weekend, the Wall Street Journal reported Parts Shortages Crimp US Factories. American factories are running short of parts. Suppliers of everything from engines to electronic components aren’t keeping up with a boom in US manufacturing, which has lifted demand in markets such as energy, mining, and construction. As a result, some manufacturers are idling production lines and digesting higher costs. As business problems go, this is a relatively good one to have. Transportation bottlenecks are often much easier to fix than lagging sales. And some of the “lost” revenue eventually comes in as companies figure out how to deliver. To me, the bigger questions are why, given all this activity, GDP isn’t growing even faster than the 4.1% initial 2Q number, and why rising transport costs aren’t yet more evident in core inflation. Yes, inflation is picking up, but not enough to make the Fed change course. Jerome Powell and crew seem content to let the economy run a tad “hot” as compensation for years of not-so-hot conditions. We are beginning to see what “hot” looks like. I think much more is possible. I am well aware of the many less-optimistic signs in the economic data. I also know personally some people for whom the 3.9% unemployment rate is not at all encouraging. They are still digging out of very deep holes, at significantly lower pay than they earned a decade ago. Likewise, I know inflation is higher than the averages reflect in many places, particularly for housing, health care, and other necessities. Everything isn’t great everywhere… but everything isn’t terrible everywhere, either. Good things are happening. We should not ignore them. Eventually, something will derail this recovery and we will enter that Great Reset period I have described. It could be a credit event, liquidity shortages, currency crisis, war, political turmoil, business scandal—the possibilities are endless. When? I now think we have another at least 1–2 years. Between now and then we could (and I hope we do!) see an economic boom that will knock your socks off. That is how economic cycles typically end. It’s been so long since we saw such a boom that even many old enough to have lived through one have forgotten what it’s like. I remember, and I don’t think we are there yet. That means we still have potentially profitable business and investment opportunities. Of course, you want to be cautious and thoughtful about seizing them. You should prepare for worse times, yes, but don’t head for the hills just yet. The above is just some of the economic and financial good news in the US. If you want really good news, look at what’s happening inside many companies and industries. The cost of solar panels is plunging, as is the cost of pulling a barrel of oil out of the ground. The energy business is now a technology business. Massive leaps are being made in 3D printing, robotics, and artificial intelligence. And not just sporadically, but in literally hundreds of businesses and universities all over the world. I know Elon Musk is a bit of a lightning rod right now, but he was visionary enough to somehow put a rocket into space, launch a satellite, and then bring that same rocket back to earth. He promises to eventually cut the cost of putting something into space by 90%. Richard Branson, Jeff Bezos, and Paul Allen are in the same race. Notice a pattern? It is not governments but committed multi-billionaires moving the human race forward. And they are doing it with the bottom line in mind. I know asteroid mining sounds like science-fiction, but there is literally a limitless amount of materials available near Earth. They are visionary enough to see it. Another billionaire, Bill Gates, has done a masterful job of focusing the world on malaria. Malaria deaths are down by 60% since the turn-of-the-century. There is still much to be done, but it’s major progress. I can cite scores of statistics (and will in my book) about how things are getting better. And they will continue to get better even as we go into The Great Reset’s financial turmoil. There are going to be so many new investment opportunities that you will almost feel like you’re being whipsawed. And because of the financial turmoil, raising capital will be more difficult, which means you will get better deals for your investment dollars. And I haven’t even begun to touch on biotechnology and the fight against aging. I truly believe cancer will be a nuisance in less than 10 years, as opposed to what is sometimes a death sentence today. There are so many new therapies coming online. I am on the board of a company whose main purpose is to eventually turn back the aging clock and allow us to live much longer and exciting lives. Cautious optimism has always been the best way to invest and is certainly the best way to live. Someday in the future, I am going to make a list of all the websites and newsletters that I get that focus on new technology. Reading a few of those a week will help lighten your mood. If you properly construct your portfolio today, you will be able to enjoy this phenomenal future. It’s going to be fun if you make the proper plans. Shane and I have a few more days in Beaver Creek relaxing and playing tourist, and Saturday we will return to Dallas to begin making some changes in my own portfolio and businesses—eating my own cooking so to speak. I have no flights actually booked, but I know at least six or seven trips are coming in the next few months. And I’m beginning to crank on my book, work on the next SIC conference in May, and many other things. I actually got out on the golf course yesterday for the first time in what seems-like-forever. While what I was doing didn’t look much like “golf” should appear, I did walk off the course without needing major pain medicine. It convinced me I might like to play golf a little more, but first I need to seriously take up yoga, spend more time in the gym stretching, and take care of myself. And with that, I will hit the send button and wish you a great week! Your really upbeat about the future analyst,   | John Mauldin

Chairman, Mauldin Economics |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.     | | Share Your Thoughts on This Article | | |

|