| By John Mauldin | Jul 19, 2017 Trade War Games “We’re already in a trade war with China. The problem is we’ve not been fighting back.” – Peter Navarro “The battle for Helm’s Deep is over. The battle for Middle Earth is about to begin.” – Gandalf the White

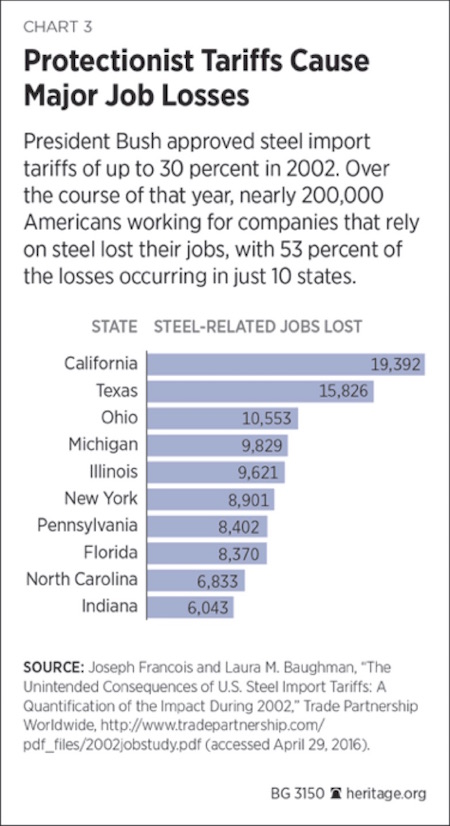

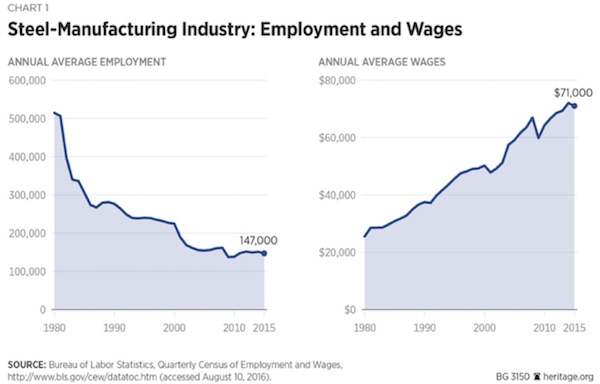

Image: Wikimedia Commons This letter should find you buckled in for the turbulence I described last week. If not, I hope this one convinces you. The storm is seven days closer now. There are times when normality slips out of reach, and I believe we are approaching such a time. I have lived through recessions and bear markets; I know what they look like. I wish I could forget what they feel like. They don’t come out of nowhere; there are always warning signs. Many investors choose to ignore those signs; I choose not to. I hope you make the same choice. The monster can come from different directions. Imagine the horror movie where the doomed victim knows the creature is out there. He hears its growls and desperately looks all around for their source. Then the camera pans left and you see the darned thing sneaking up on him from behind. [Cut, add scream, fade to black.] Over the next few letters we will consider the various monsters that may set upon us. Any one on its own might be manageable, but we’ll be out of luck when several hit us in rapid succession. We’ll start with this big bad boy: Trade War. For the last 20 years, the biggest monster in my worry closet has been protectionism and trade wars. Last year both presidential campaigns voiced ideas about protectionism and trade that reflected appalling economic ignorance about the importance of trade to global prosperity, and particularly to the prosperity of the US. As I explained in “The Trouble with Trade,” I hoped then that the talk was all just campaign rhetoric and political pandering. No such luck. Comparative Advantage Trade is the global economy’s bloodstream. The more freely it flows, the better for all. As David Ricardo explained 200 years ago, different peoples have unique characteristics that enable them to produce certain goods at lower opportunity costs than other can. Free trade gives consumers access to the best goods and services at the lowest prices. However, what we now call “free trade” is not what Ricardo had in mind. We have instead managed trade designed to benefit certain favored parties and to disadvantage others. You can’t blame free trade for our problems, because we haven’t got it. Those who have seen their interests short-changed in the managed-trade game have had enough. That’s one reason Donald Trump is now president and anti-globalization movements are active in so many countries. Candidate Trump talked about renegotiating trade agreements to help American workers. I support that goal. The problem is that President Trump seems intent on starting a trade war that will hurt those same workers. We are on a very dangerous course. Worse, if a report I saw last week is accurate, that course is already locked in. Consequential and Contentious The report comes from Axios, a Washington-based news site recently launched by some Politico veterans who want to disrupt the mainstream media. This is what Axios reported June 30, based on the input of anonymous Trump-administration sources: With the political world distracted by President Trump’s media wars, one of the most consequential and contentious internal debates of his presidency unfolded during a tense meeting Monday in the Roosevelt Room of the White House, administration sources tell Axios.... With more than 20 top officials present, including Trump and Vice President Pence, the president and a small band of America First advisers made it clear they’re hell-bent on imposing tariffs – potentially in the 20% range – on steel, and likely other imports.... One official estimated the sentiment in the room as 22 against and 3 in favor – but since one of the three is named Donald Trump, it was case closed. No decision has been made, but the President is leaning towards imposing tariffs, despite opposition from nearly all his Cabinet. The following Sunday, July 2, the Wall Street Journal’s William Mauldin (no relation to me) filed this: The Trump administration missed a self-imposed Friday deadline for concluding a major probe of steel imports, a delay officials said was driven by unanticipated complexities in engineering such a big shift in U.S. trade policy. The administration has faced challenges in implementing its “America First” policy amid resistance from lawmakers and many business groups who worry that new curbs on steel imports could drive up costs for American manufacturers and spark retaliation from trading partners. That report suggests that the June 26 meeting was less conclusive than Axios opined – but the trade hawks have not given up. The “America First” side is probably headed by presidential advisor Steve Bannon and Peter Navarro, director of Trump’s National Trade Council (a new office created by Trump), along with Trump himself. Navarro, a former University of California, Irvine economics professor, was already a well-known protectionist when Trump hired him as a campaign advisor last year. Author of a book called Death By China, he is opposed to trade deficits and has accused China and Germany of currency manipulation. Very few academic economists share Navarro’s views. The simple fact is that Navarro embraces fallacious economics ideas. Kevin Williamson in the National Review takes his measure: Professor Navarro, among other things, makes economics errors that would be obvious to an undergraduate. This has been commented on at some length elsewhere, most prominently after he published a review of the Trump economic plan (a review co-authored with Wilbur Ross, who is not an economist but is now Secretary of Commerce) in which he proffered the schoolboy argument that, because GDP is defined as the sum of consumption, investment, government spending, and net exports, eliminating our trade deficit with China would add substantially to GDP. In economics terms, he has mistaken an accounting identity for real-world causality; in layman’s terms, this is horsepucky, “a mistake that an econ professor like him really shouldn’t be making,” as Noah Smith of Bloomberg put it. This is an appalling mistake for anyone, but for an economics professor to do this? And one that is actually in a position to influence trade policy? In his books and writings, Navarro peddles analogies he pulls out of thin air as “facts,” without a shred of evidence to back them. For instance, as Williamson notes, His sloppiness with sources is general. Navarro cites a Rand Corporation report suggesting that China is behind Iran’s nuclear program without mentioning that the report is a quarter-century old, that it identifies China as a “moderate threat to U.S. interests,” or that subsequent Rand analysis suggests that Chinese involvement with Iranian nuclear ambitions seems to have ended around 1997. He does not even cite any particular Rand report, simply attributing a long quotation to “the Rand Corporation.” Navarro makes up stories about a future where poorly made Chinese cars are crashing and killing US citizens (even though a few extraordinarily well-made Volvos are the only cars made in China that are driven in the US). He claims that the Chinese keep unemployment high so that wages can remain low, even though their wages have been rising significantly for the last 15 years. Professor Peter Navarro and the ideas he espouses are dangerous. Certainly, we can be smarter about how we negotiate trade deals in order to get the best terms possible. Peter Navarro is simply not the man to be advising on that. Most leaders of larger businesses have no interest in truly free trade, either, but they dislike Navarro’s ideas. There is a stand-off within the administration. The battle pits trade advocates and businesspeople vs. Bannon and Navarro. Trump apparently leans Bannon and Navarro’s way but hasn’t made a final decision yet. The proposed steel tariffs are more significant than they may seem. A Commerce Department study is trying to determine whether imported steel represents a national security threat to the US. If so, a 1962 law gives the president vast powers to impose tariffs and other barriers, without congressional approval. If Trump wants to start a trade war, Congress and the courts probably can’t stop him unless they can pass new laws by a veto-proof margin. The chances of that happening are near zero. That meeting in the Roosevelt Room may turn out to be as consequential as Bretton Woods was, if Trump acts to launch major trade sanctions. Trade sanctions will slow down already slow global economic growth and could trigger a much wider systemic crisis. What Would Steel Tariffs Really Mean? It makes a difference whether the administration decides to impose quotas on current steel imports or initiate a tariff. Quotas would be harmful, but a tariff would be far worse. Let’s look at who would actually be damaged. First, for all the talk about trade deficits with China, we don’t import all that much steel from China. In fact, China isn’t even in the top 10 countries that we import steel from, as shown in this chart from the Financial Times:  Secondly, using national security as an excuse to impose tariffs is really fraught with potential problems. The Financial Times report (well worth reading) in which our chart appears notes two: The first is that in the trade realm, invoking national security to erect barriers is considered a nuclear option. World Trade Organisation rules include a national security exemption designed to be used in times of war. But many experts believe the forthcoming steel move would flout those rules and would thus be challenged by other WTO members. Such a challenge in itself could be dangerous. It would be the first real test of the WTO’s national security exception. Were the WTO to find against the US and the Trump administration to ignore that decision, it would be a huge blow to the WTO’s credibility. Were the WTO to find in the US’s favour experts fear it could give carte blanche to all WTO members to invoke national security more often, leading to a new protectionist free-for-all. The second is that the US is the world’s largest steel importer and a broad move on steel would probably hit US allies such as Canada, Germany, South Korea and Mexico far more than China, its real intended target. In an unusual move, it has prompted Nato allies to complain and to try to have the Pentagon lobby on their behalf. It also could provoke a messy trade war with other countries feeling compelled either to impose their own national security restrictions on steel imports or to retaliate against the US in other ways. The third reason to oppose tariffs is that clamping down on steel imports threatens considerably many more jobs than “protecting” the steel industry from foreign competition can save. As Dan Pearson of the Cato Institute noted recently: “Steel mills employ 140,000 workers. Manufacturers thatâ¯use steel as an input 6.5 million, 46 times more.” Steel mills’ $36 billion of productivity in 2015 represented just 0.2 percent of USâ¯GDP, Pearson explains, while the economic value contributed by US firms that use steel wasâ¯29 times larger. We actually have a recent case study. George W. Bush approved steel import tariffs of 30% in 2002. What happened? Two hundred thousand American workers lost their jobs, as this chart from the Heritage Foundation illustrates.  Scores of different types of steel are used for special manufacturing processes and equipment. The US doesn’t manufacture everything we need or have the capacity to do so. Thus a tariff would increase costs to consumers without doing one thing for steelworkers. Yes, the number of American steelworkers is down from 500,000 to 147,000 in the last 35 years. As in so many industries, we simply don’t need the number of workers that we used to. Steelworkers, whose wages have tripled, are producing five times the amount of steel per hour worked as they did 35 years ago.  China is already working to curb its steel production capacity, as demand for steel is flat to down. Now I agree that Chinese overproduction is forcing global steel prices down, but do we really have a problem when gasoline prices go down? Do we feel sorry for the oil companies? No doubt American steelworkers and steel companies would love to see barriers to entry for their product. I bet McDonald’s would like to have Jack-in-the-Box stores banned, too. Ultimately, higher prices offset the theoretical benefits of a steel tariff or quota. You and I are the ones who pay. Buy American The federal government has other ways to punish foreign competitors. In April President Trump visited the Wisconsin headquarters of Snap-on Tools, where he signed a “Buy American, Hire American” executive order. The bureaucracy is now working to implement the order. Laws dating back to the Great Depression require federal agencies to give first preference, in government contracts, to US-made products. Over time, it became routine for acquisition officers to grant waivers to those requirements. President Trump’s order will crack down on those waivers. This will soon be evident at the Pentagon, where two laws apply: The two laws in question are the 1933 Buy American Act, which requires the Pentagon to purchase domestically produced products for purchases over a $3,500 threshold, and the more-restrictive 1941 Berry Amendment, which applies mainly to clothing and food products purchased by the military. Together, these laws ostensibly require that the U.S. military’s entire supply chain be sourced from inside the country…. By enforcing these laws, President Trump can redirect billions of dollars in spending from foreign companies to US suppliers – assuming US suppliers exist. They may not, in some cases, and they may cost more if they do. Defense contractors will face some serious headaches.

AP Photo Other trade actions are popping up, too. Boeing has asked the government to investigate what it considers to be unfair competition by Bombardier, a Canadian aircraft manufacturer. If Boeing succeeds in sidelining Bombadier, other US companies are likely to make similar claims. But, truth is, dozens of countries manufacture major parts of those Boeing airplanes; Boeing doles out contracts to other countries in order to encourage them to buy the planes. Many of those components are made in Canada. And I will bet you a dollar to 47 doughnuts that significant components of Bombardier planes are made in the United States by US workers. It behooves us to remember that Canada and all our other trade partners have options, too. Tit for Tat The trade war, if it happens, will spring from the administration’s failure to appreciate one simple fact: Other countries will respond. The Trump administration’s steel tariff idea, for example, has already provoked European Union officials. EU trade commissioner Cecilia Malmstrom warns, “We want of course to avoid anything dramatic here but if that would have hit our companies we will have to respond, of course.” The EU and other trade partners will not simply roll over and accept US tariffs. They will retaliate in ways specifically calculated to hurt American businesses and consumers. My fear is that the US will then up the ante with yet more tariffs or other barriers, and the fight will get ugly, causing real pain and losses for both sides. All this will be completely unnecessary. Can existing trade agreements be improved? Yes, definitely. But trade negotiations are insanely complex in the best of circumstances. Multiplayer game theory applies. Right now we have general trade equilibrium, with minor adjustments all the time. Not everyone has everything they want, but no one is angry enough to stop playing. If one major player changes the rules, however, all the other players in the game have to respond. Those national players have their own businesses and voters that they must pander to. The game can collapse quickly. Pile that risk on top of our many other economic vulnerabilities, such as the increasing political turmoil in Europe, and we might see major fireworks. President Trump campaigned on the promise that he would negotiate better deals. Well then, Mr. President, rather than impose tariffs and destroy a few hundred thousand high-paying jobs in US manufacturing, let’s find out how well you can negotiate. And send Professor Navarro, whose supposed expertise is in utilities, of all things, back to California. Before I close, I want to announce that we’re hosting another webinar with my friend Marc Chaikin of Chaikin Analytics, on July 25, at 4:15 PM EST. I’ve long been a fan of the Chaikin Analytics Power Gauge, so last year I told my team of analysts to try it out. A few weeks later they came back to me and said, “It’s great, we’re using it for everything!’’ Because we’re so impressed with the Power Gauge system, we’d like to give you the opportunity to access it, too. You can click here for the free webinar “The Ultimate Stock Checklist & Best Small-Cap Stocks to Buy Today.” Grand Lake Stream, Colorado (?), and Lisbon Shane and I will be going to Las Vegas next week for Freedom Fest, then we’ll come back home to Dallas for a few weeks before I’m off to Grand Lake Stream, Maine, for the annual economics schmooze and fishing trip known as Camp Kotok. Afterward, I am thinking about going to somewhere in Colorado for a few days to escape the Texas heat. There are a lot of potential trips in September, but the next outing now on the books will be to Lisbon, Portugal. Over the weekend what was going to be a short family meeting turned out to be much lengthier and much happier than I envisioned. As a result, this letter is coming to you later than usual. (Sometimes life just happens when you’re making plans.) I hope you, too, have an unexpectedly wonderful week. Your hoping we walk away from protectionism analyst,

John Mauldin

subscribers@MauldinEconomics.com Copyright 2017 John Mauldin. All Rights Reserved. | Get a Bird’s-Eye View of the Economy with

John Mauldin’s Thoughts from the Frontline

This wildly popular newsletter by celebrated economic commentator, John Mauldin, is a must-read for informed investors who want to go beyond the mainstream media hype and find out about the trends and traps to watch out for. Join hundreds of thousands of fans worldwide, as John uncovers macroeconomic truths in Thoughts from the Frontline. Get it free in your inbox every Monday. |

Share Your Thoughts on This Article

http://www.mauldineconomics.com/members Thoughts From the Frontline is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com. Any full reproduction of Thoughts from the Frontline is prohibited without express written permission. If you would like to quote brief portions only, please reference www.MauldinEconomics.com, keep all links within the portion being used fully active and intact, and include a link to www.mauldineconomics.com/important-disclosures. You can contact affiliates@mauldineconomics.com for more information about our content use policy. http://www.mauldineconomics.com/subscribe Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President and registered representative of Mauldin Solutions, LLC, a registered investment adviser with the US Securities & Exchange Commission and states unless an exemption is available, President and registered representative of Mauldin Securities, LLC, (MS) member FINRA and SIPC, through which securities may be offered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee. Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Mauldin Securities. It is intended solely for investors who have registered with Mauldin Securities and its partners at www.MauldinCircle.com (formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Mauldin Solutions, LLC, a registered investment adviser with the US Securities & Exchange Commission and states unless an exemption is available. John Mauldin is a registered representative of Mauldin Securities, LLC, (MS), an FINRA registered broker-dealer. Mauldin Securities cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements. PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273. |