Inflation Watch: Core high, headline to rise further

Click here for full report and disclosures

Click here for Inflation Watch slides

*All measures of inflation have accelerated. CPI inflation has risen to 7.9% yr/yr and 6.4% excluding food and energy. PCE inflation has risen to 6.1%, and 5.2% on its core. Producer price indexes are rising even faster. Inflation is the highest since the early 1980s.

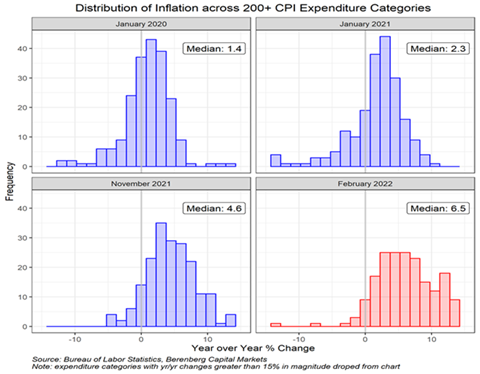

*Our detailed analysis of price increases of over 200 components of the CPI indicates a further widening distribution of accelerating price increases across goods and services (See Chart 1). The portion of CPI components experiencing inflation above 3% and above 5% are similar to the early 1970s, but not yet as high as the late 1970s.

*Average hourly earnings (AHE) increased 5.1% yr/yr in February, but real wages are declining. Extremely tight labor markets and the feedback of inflation on wages should keep nominal wage increases elevated.

*Inflationary expectations for the near and intermediate term are quite high according to both survey and market-based measures. Market-based measures of longer-run inflationary expectations between 6-10 years remain only moderately above the Fed’s longer-run 2% average target.

*The negative supply shock stemming from the rise in oil and commodity prices will boost headline inflation in coming months. While core inflation seems to be showing signs of peaking, elongated constraints on supply and higher inflation may push up inflationary expectations and inhibit desired declines in core inflation.

Chart 1: Distribution of inflation across CPI components

Mickey Levy, mickey.levy@berenberg-us.com

Mahmoud Abu Ghzalah, mahmoud.abughzalah@berenberg-us.com

© 2022 Berenberg Capital Markets, LLC, Member FINRA and SPIC

Remarks regarding foreign investors. The preparation of this document is subject to regulation by US law. The distribution of this document in other jurisdictions may be restricted by law, and persons, into whose possession this document comes, should inform themselves about, and observe, any such restrictions. United Kingdom This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers. Copyright BCM is a wholly owned subsidiary of Joh. Berenberg, Gossler & Co. KG (“Berenberg Bank”). BCM reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the BCM’s prior written consent. Berenberg Bank may distribute this commentary on a third party basis to its customers.