U.S. PCE inflation remains elevated, while consumption weakened in July

*Today’s Report on Personal Income and Consumption for July provides a clear signal that real (inflation adjusted) consumption has flattened, while inflation continues to rise. Although strong job gains and rising wages are boosting gains in personal income, real spending has slowed, presumably reflecting supply constraints and higher product prices, and inflation shows no signs of decelerating.

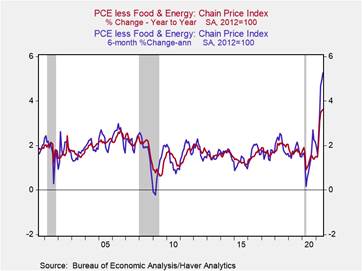

*PCE inflation 0.4%, lifting its yr/yr rise to 4.2%, while core PCE inflation excluding food and energy rose 0.3%, leaving its yr/yr rise at 3.6% (Chart 1). These inflation measures are not showing signs of easing: the 6-month annualized rises accelerated to 5.9% on headline PCE inflation and 5.25% on the core PCE price index (Chart 2). These are dramatically higher than earlier forecasts by the Federal Reserve and most private forecasters pose the notion that the inflation is temporary. We note that the monthly increases in the PCE price index were quite low in the last five months of 2020 (they averaged 0.18% per month on the headline PCE and 0.16% on the core), pointing toward further increases in the yr/yr inflation measures.

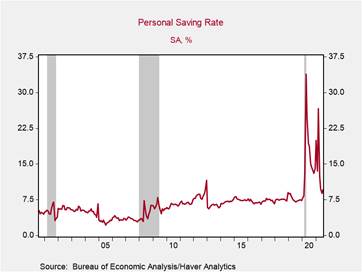

*The 1.1% rise in disposable personal income and the 0.3% increase in consumption involved a rise in personal savings and an increase in the rate of personal savings to 9.6% from 8.8% (Chart 5).

Chart 1: PCE chain price index and PCE less food & energy

Chart 2: PCE less food & energy year-over-year and 6-month change annualized

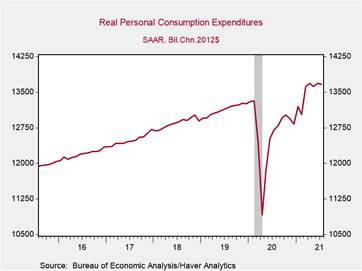

Chart 3: Real PCE

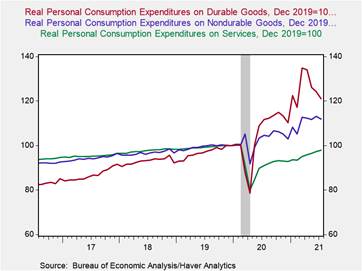

Chart 4: Real PCE on durables, nondurables, and services

Chart 5: Personal savings rate:

Mickey Levy, mickey.levy@berenberg-us.com