Click here for full report and disclosures

â  A highly unusual downturn: Despite the massive GDP shock from the pandemic during the past year, UK underlying private demand remains firm thanks to the governmentâs wide range of fiscal initiatives to support household incomes. The unusual combination of strong incomes but weak spending under lockdowns and other such virus restrictions has led to a major surge in household saving.

â  How much extra saving? We estimate that households accumulated around £193bn in excess savings from Q1 2020 to Q1 2021, worth c14% of 2019 nominal household consumption. The saving ratio peaked at 25.1% in Q2 2020 â almost double the post-financial crisis peak of 12.7% in Q1 2010. This large âexcessâ over and above the usual precautionary element that is normal during a downturn represents involuntary saving and can add to demand over time.

â An uneven shock: Since Q1 2020, restrictions to control the spread of SARS-CoV-2 have determined consumption patterns much more than underlying demand and the fundamentals underpinning it. Restrictions hurt spending on face-to-face services much more than goods consumption, which can more easily shift online.

â  Robust fundamentals: Unlike the situation after the 2008/2009 financial crisis, most households are coming out of the COVID-19 downturn with healthier finances and stable employment income. Supported by a huge reservoir of excess demand due to the savings surge, strong underlying fundamentals can turn into sustained gains in spending after a rapid near-term recovery as restrictions are eased.

â  Rebalancing ahead: The uneven shock to spending during the past year will likely be reversed during the rebound. Recovering spending on transport, restaurants, hotels and leisure should more than offset modest likely dips in spending on food, household furnishing and other categories that have spiked during lockdowns.

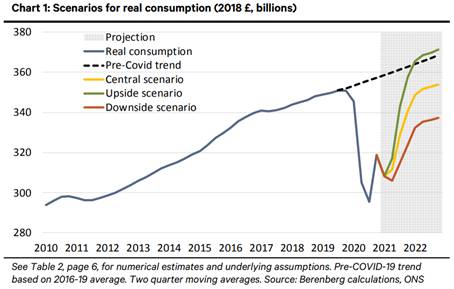

â Potential scenarios: Due to still elevated pandemic uncertainties, a wide range of outcomes remains possible â Chart 1. In our central scenario, real private consumption is c1% higher by Q4 2022 than in Q4 2019 â it is c6% higher in our upside scenario and c4% lower in our downside scenario. Although real consumption exceeds the pre-pandemic level in our central scenario, by the end of Q4 2022 it remains below the pre-COVID-19 trendline. This mostly reflects the loss of income growth during the pandemic. Judging by the robust state of underlying fundamentals, we judge that medium-term risks are skewed towards our upside scenario. Rebounding confidence suggests that households are eager to spend.

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659

Joh. Berenberg, Gossler & Co. KG is a Kommanditgesellschaft (a German form of limited partnership) established under the laws of the Federal Republic of Germany registered with the Commercial Register at the Local Court of the City of Hamburg under registration number HRA 42659 with its registered office at Neuer Jungfernstieg 20, 20354 Hamburg, Germany. A list of partners is available for inspection at our London Branch at 60 Threadneedle Street, London, EC2R 8HP, United Kingdom.

Joh. Berenberg, Gossler & Co. KG is authorised by the German Federal Financial Supervisory Authority (BaFin) and deemed authorised and regulated by the Financial Conduct Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authorityâs website. For further information as well as specific information on Joh. Berenberg, Gossler & Co. KG, its head office and its foreign branches in the European Union please refer to http://www.berenberg.de/en/corporate-disclosures.html.