Click here for full report and disclosures

â Some signs of hope: Ongoing UK-EU negotiations for a comprehensive future relationship have turned more amicable of late. Although the UK has firmly refused to extend the transitional period beyond 31 December 2020, both sides are floating potential compromises that can unlock other areas of difference such as on governance, level playing field provisions and politically sensitive fisheries.

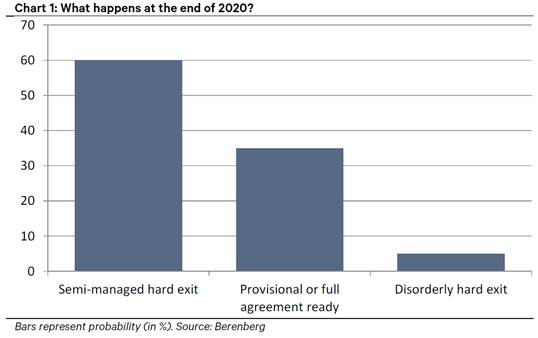

â Our base case remains unchanged: Despite signs of progress, we still do not expect a deal in time for the year-end. Instead, we expect the two sides to agree on some modest stopgap measures in order to prevent a disorderly hard exit. Instead of one big cliff edge, where the UK-EU economic relationship suddenly shifts from open single market rules to the much more restrictive World Trade Organisation rules for trade, we expect the two sides to see to it that the switch occurs in a series of smaller steps. We put a 60% probability on this outcome.

â Positively skewed risks: We no longer see a disorderly exit as the major risk – and most likely alternative – to our base case. Instead, we see a reasonable chance (35%) that the two sides can strike a deal worth its name before the end of the year. On the downside, we see a 5% tail-risk of a disorderly hard exit.

â Irish border – still the critical issue: Earlier this year, the UK government had stated that it would not perform checks on goods flowing between Great Britain and Northern Ireland, thereby violating the legal commitments it made in the Withdrawal Agreement that will prevent a hard border returning to the island of Ireland. However, more recently, things have taken a turn for the better. The UK now accepts that it will need to perform such checks. The progress on this critical issue seems to have helped to break the deadlock in other key areas.

â Politic context matters: While the pandemic has not affected the UKâs desire for a deal as much as is commonly perceived and the EUâs flexibility on what it can agree remains limited, there seems to be some scope for both sides to strike acceptable trade-offs in order to conclude a deal. Still, a lot has to go right for that to happen by the end of the year.

â Economic outlook: Our call for a tick-shaped recovery from the COVID-19 mega-recession hinges on the UK avoiding a disorderly hard exit. In such an outcome, the UK could temporarily fall back into recession in early 2021. Conversely, a full or partial deal by the end of the year or in early 2021 would tilt the medium-term growth risks to our UK forecasts to the upside.

We invite you to join us on Thursday 2 July to discuss these issues in more detail via conference call – see attached invites

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

Chief Economist

+44 20 3207 7889

holger.schmieding@berenberg.com

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659