Click here for full report and disclosures

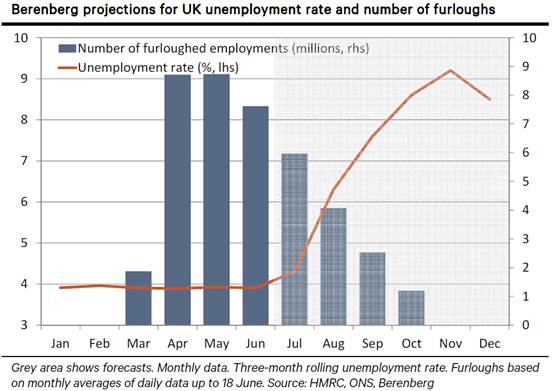

â  Aggressive action works: The UKâs Coronavirus Job Retention Scheme (CJRS), which was rolled out in March, continues to work well. Through the scheme, firms can claim up to 80% of a furloughed employeeâs pay (capped at £2,500 per month). The UK unemployment rate remained at just 3.9% in June, unchanged from its pre-COVID level, despite the 25.6% plunge in GDP between February and April during the national lockdown.

â  Recent furlough trends: In early May, subsidy claims peaked at 8.86m employments. Latest data available up to the 18 June shows that this number has fallen to 7.49m. Since 1 July, workers can be brought back on a part-time basis while firms claim subsidies for part of the shortfall in hours. While this supports the employment recovery as output rebounds, as a best guess, we estimate that claims declined to 5.97m in July before falling to 4.1m in August.

â  Unemployment likely to rise sharply soon: Before the CJRS ends on 31 October, the degree of subsidy will be reduced in September (70% with a cap of £2,187.50) and again in October (60% with a cap of £1,875). This will encourage firms to make the tough choices as to whether to bring workers back on a permanent basis or make redundancies. Recent newsflow suggests a wave of layoffs is underway. Having remained stable through to June, we expect the incoming data to show that the unemployment rate started to rise in July. This will continue in the months to come. Unemployment is likely to peak in November â the first month after the CJRS expires â or shortly thereafter.

â  How high will unemployment peak? Key labour market data such as employment and unemployment, which are currently distorted by the CJRS, may only adjust fully once the scheme ends. With no recent data trends to go on, forecasting the potential peak rate of unemployment is tricky, to put it mildly. As a guide, we assess the historical relationship between the unemployment rate and real GDP â Okunâs rule. Real GDP roughly 6.8% below its pre-COVID level (our Q4 projection) suggests that the unemployment rate will peak at around 9.2% towards the end of the year.

â  The âSchumpeterâ philosophy: Many commentators argue that the UK should extend the furlough scheme beyond October to delay the correction in the labour market. Both Germany and France have decided to extend their schemes into 2021. The UK government does not seem to share this view. Instead, it wants to avoid artificially locking workers into unproductive jobs. The pandemic has accelerated the long run shift away from face-to-face retail and professional services towards online commerce and remote working. While reallocating workers into more productive jobs as swiftly as possible makes economic sense from a long-run perspective, it carries a serious risk with it. A big labour market wobble at the end of the year could hurt confidence further and disturb the fragile recovery that is still vulnerable to virus-related risks and the tail risk of a disorderly exit from the single market at year-end.

â  Another policy U-turn? While it is not our base case, we see two potential developments that could force the government to have a last-minute change of heart and extend the CJRS, at least for the worst hit sectors such as food services, accommodation and travel: first, if the number of potential layoffs once the scheme ends is intolerably high â ie such that it risks pushing the unemployment rate into the mid-teens; second, in case of a major second wave of the pandemic that leads to a second national lockdown or a tightening of restrictions by enough to stall the rebound.

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659

Any e-mail message (including any attachment) sent by Berenberg, any of its subsidiaries or any of their employees is strictly confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received such message(s) by mistake please notify the sender by return e-mail. We ask you to delete that message (including any attachments) thereafter from your system. Any unauthorised use or dissemination of that message in whole or in part (including any attachment) is strictly prohibited. Please also note that any legally binding representation needs to be signed by two authorised signatories. Therefore we do not send legally binding representations via e-mail. Furthermore we do not accept any legally binding representation and/or instruction(s) via e-mail.

In the event of any technical difficulty with any e-mails received from us, please contact the sender or info@berenberg.com.

Click here to unsubscribe from these emails.