At the conclusion to its June 9-10 FOMC meeting, the Fed’s Policy Statement emphasized that it is committed to maintaining its expansive monetary policies to promote its maximum employment and low inflation goals, and Fed Chair Powell emphasized that the Fed is monitoring conditions closely and is prepared to use its full range of policy tools necessary to support the economy.

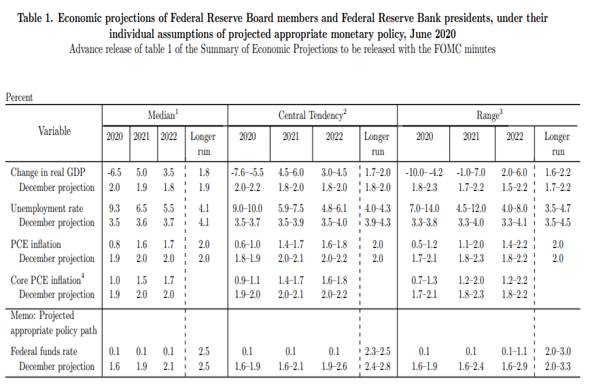

*The FOMC voted unanimously to maintain its Federal funds rate target at 0%-0.25%. In its Summary of Economic Projections (SEPs), the median FOMC member’s estimate of the appropriate Fed funds rate was unchanged at 0%-0.25% through year-end 2022.

*The Fed committed to continued increases in its balance sheet through ongoing purchases of Treasury and mortgage-backed securities (MBS) and commercial MBS at its recent pace.

*The Fed’s Policy Statement did not mention its lender of last resort policies of purchasing corporate bonds and municipal debt or its direct business lending program.

*In its SEPs, following the sharp contraction in real GDP and spike in unemployment and disinflation, the FOMC members projected a solid economic rebound and decline in the unemployment rate and a rise in inflation toward, but not reaching, its 2% target by year-end 2022.

In his press conference, Fed Chair Powell emphasized the high degree of uncertainty in the economy and signaled that the Fed stood ready to use its vast monetary tools as necessary to support the economy. In response to the Fed’s Policy Statement, SEPs and Fed Chairman Powell’s remarks at the press conference, Treasury bond yields receded and the U.S. dollar added to its recent decline.

After skipping its March SEPs, the Fed’s updated June projections forecast a solid economic recovery, with real GDP growing 5% in 2021 (measured Q4/Q4) and 3.5% in 2022, and a decline in the unemployment rate to 9.3% by year-end 2020, 6.5% by year-end 2021, and 5.5% by year-end 2022. These estimates suggest that by year-end 2022 the Fed projects real GDP will have regained its Q4 2019 level but the unemployment rate will remain well above its pre-pandemic 3.5% level.

The Fed estimates that core PCE inflation will be 1.0% at year-end 2020, reflecting its temporary bout of disinflation, and will rise to 1.5% by year-end 2021 and 1.7% by year-end 2022. In light of the Fed’s pursuit of its maximum employment objective and its symmetric 2% inflation objective, this forecast provides the Fed ample flexibility to remain expansively easy.

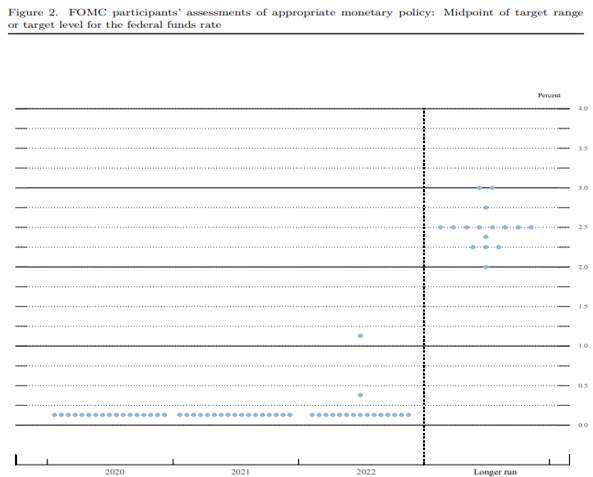

In the Fed’s “dot plot,”--the plots of each FOMC member’s estimate of the year-end Fed funds rate target most appropriate with their individual economic and inflation forecasts--only two members estimated that it would be appropriate to raise rates from its current level of 0%-0.25% by year-end 2022

Source: Board of Governors of the Federal Reserve System

Source: Board of Governors of the Federal Reserve System

Mickey Levy, mickey.levy@berenberg-us.com