| Steve's note: As regular readers know, I believe this market has plenty of upside ahead as we approach its "climactic third act." But today's essay offers a different perspective. We're sharing another excellent piece from investment-newsletter legend Jim Grant... Originally published on July 28, it's a thorough examination of a "most unusual" bull market. I hope you enjoy it...

| What to Do With Money Today... Besides Enjoy It | | By Jim Grant, editor, Grant's Interest Rate Observer | | Friday, October 6, 2017 |

| "Short Sellers Retreat Amid Rally," ran the headline in the Wall Street Journal.

Curious readers stopped and stared. It was the premise of the headline that arrested them. Who knew that there was even one bear left to give ground at the 100-month mark of the post-2008 levitation?

El toro is the topic at hand. It's a most unusual bull market (we count as one the updrafts in stocks and bonds). An unzestful, low-volume, and low-volatility affair, it seems to belong on a psychiatrist's couch. We write to catalogue its singularities with the purpose of addressing the always pertinent question: What to do with money besides enjoy it?

----------Recommended Links---------

| Porter wants to give you a $1,000 credit

There's a nifty way readers could've TRIPLED the returns of Stansberry's Investment Advisory... and nearly QUADRUPLED the returns of True Wealth. That's why once you decide you can't live without this simple tool, we'll send you a $1,000 credit! Click for details. |

|---|

---------------------------------

No. 1 is the zest deficit. Since the S&P 500 Index bottomed at an intraday low of 666.79 on March 6, 2009, the blue chips have appreciated by 271%. The country has grown, too, although – famously – the economic expansion leaves much to be desired. Trailing 12-month earnings for the S&P 500 peaked in the third quarter of 2014, and disappointments abound in the data that purport to measure growth in GDP and productivity.

Still, you'd expect more joie de vivre. There's little enough on Wall Street, where the price war in money management spells profitless prosperity for the leaders in index funds and exchange-traded funds (ETFs).

Not that the remnant of surviving active managers appears any happier than the index administrators. According to Bank of America Merrill Lynch's Global Fund Manager Survey for July, non-indexed investors are the least committed to (the "most underweight") American equities since the start of 2008.

A second singularity of the 2009-2017 bull market is the shrunken level of the activity that sustains it. In the year to date, the S&P 500 has traded an average of 565 million shares a day, down from a daily average of 642.2 million last year and 1,290.5 million in 2007.

Trading in bonds, currencies, and commodities has similarly dwindled (at least, as recently reported by JPMorgan Chase and Goldman Sachs). "This is the only multiyear bull market in history whereby trade volumes are declining rather than increasing," says Christopher Cole, founder of Artemis Vega Fund.

A perhaps related anomaly is the dwindling population of American investor-owned businesses. In 2007, there were 4,783. As of Monday, there were 3,982. Private-equity firms are swallowing listed companies whole.

El toro's third unique feature is the undifferentiated nature of the advance. "At the March 2000 peak of the (first) Internet bubble," observes our Deputy Editor Evan Lorenz, "the capitalization-weighted S&P 500 traded at 30.6 times trailing earnings, while the equal-weighted S&P – in which all stocks count for the same, their market cap notwithstanding – traded at 20.7 times.

"There is no such dispersion today within the blue-chip index," Lorenz goes on, though there is plenty among the stocks and bonds that are too small to catch the bids of the index buyers. "Apple (AAPL), Facebook (FB), Alphabet (GOOGL), and Amazon.com (AMZN) trade at 17.9, 43.7, 31, and 195.2 times trailing earnings, respectively, and command an aggregate market cap of $2.4 trillion, which represents 11% of the S&P 500's total value. In light of these magnitudes, it isn't so surprising that the cap-weighted index changes hands at a lofty 21.7 times trailing earnings. What is surprising is that the S&P 500 Equal Weighted Index trades at 21.8 times.

"Either way, or both ways, according to the cyclically adjusted price/earnings ratio (which compares the price of the index to its average inflation-adjusted earnings over the prior decade), today's S&P is the third most expensive in U.S. history, trailing only 1929 and 1997–2001."

Central-bank-sponsored miniature interest rates and the runaway success of indexed investing, we count as singularities Nos. 4 and 5. Ultra-low rates coax income-seeking investors into the stock and bond markets. They invest because cash equivalents and short-dated savings instruments yield them nothing. But the buyer of an S&P 500 index fund is – must be – indifferent to valuation; he or she is buying the market. Even the nominally value-sensitive investor is likely to be ill-informed as to the real worth of the securities that stock his 401(k).

Corporate managements and ETF sponsors independently misrepresent valuation; it's a decentralized effort of many minds and hands. Let's call it singularity No. 6, while acknowledging that "profit" is ever a defined term. But today, there are more definitions than ever. "'Adjusted' earnings are the standard nowadays," Lorenz points out. "They exclude restructuring charges, one-time items, and other expenses which management deems to be non-recurring. The longer the bull market lasts, the more inventive do managements become at finding costs that can be designated as such...

"Adjusted figures, rather than the ones calculated according to generally accepted accounting principles, are the default setting on Bloomberg," Lorenz goes on. "Check out Kraft Heinz (KHC)... Bloomberg shows KHC trading at a trailing price-to-earnings ratio of 25.9 times. Using audited GAAP numbers, the stock is priced at 31.1 times.

"Bloomberg shows the S&P 500's price/earnings multiple as the aforementioned 21.7 times. Using the as-reported earnings data from S&P Dow Jones Indices, the S&P 500 is actually priced at 24.7 times trailing earnings."

Low volatility is as much a marker of the post-2008 bull market as is low turnover or high valuations. It's our singularity No. 7. The CBOE Volatility Index (or "VIX"), a measure of implied volatility on one-month options on the S&P 500, today stands at 9.4, below its long-term average of 19.5. In the 27-and-a-half years of its existence, the VIX has closed below 10 only 25 times, and 16 of those somnolent readings have occurred since May.

You can explain the plunge in implied volatility by observing the still more precipitous fall in realized volatility. Here the readings are less than seven. There has been no period so financially still since 2006 (and, before that, the years 1995, 1964, and 1952), according to the afore-quoted Christopher Cole.

"The problem," Cole continues, "is that by definition [volatility] can never go to zero, but it can – and has – gone to 100. When people short volatility, what they don't realize is they are actually shorting variance [i.e., the spread between numbers in a data set], which has a non-linear return profile. You have a very limited gain shorting volatility from 10 to 5. You have a very large, non-linear loss profile if [volatility] and by-proxy variance move from 10 to 100."

It's a comic conundrum that the most volatile commander-in-chief should preside over the least volatile stock market, but Donald J. Trump has so far achieved it. With volatility falling, the price of the Big Board-listed security on which one can wager on a rising VIX – its ticker is VXX – has been sawed in half this year. Volatility bears have sold short 63% of VXX shares outstanding.

Our seven singularities describe a low-volume, low-conviction, low-energy stock market (FAANG stocks being the notable exception). In the context of a standard, three-act bull-market drama, the tone perhaps resembles an inconclusive second act more than a climactic third. Maybe the sound and fury and the ultimate upside are yet to come. On the question of how high is up, we yield to the technicians.

What to do with money, besides enjoy it? A question with no correct answer, of course. For ourselves, we like neither the stock market nor the bond market and abominate the prevailing monetary arrangements. If we are confident about anything in the future, it's that bargains and tumult will return.

Professional investors, being paid to invest, can't just do nothing, as profitable as that course of action might ultimately prove. For the rest of us, we must decide if tomorrow's opportunities might not be more interesting than today's. For those who reply, "Yes, they very well might be," and who have the luxury of time and the gift of patience (and who share our foreboding about modern money), a modified Scrooge McDuck portfolio could be the thing: Heavy in cash and gold, light in inflated stocks and bonds.

Regards,

Jim Grant

Editor's note: Jim's exclusive conference is right around the corner. And Porter Stansberry has arranged a red-carpet, VIP-level invitation for Stansberry Research readers... for about half the regular price. You'll hear from some of the world's most important minds in finance. But be warned – Jim may never offer anything like this again. Get the details right here. |

Further Reading:

Renowned investors like Jeremy Grantham have said "this time is different" – or at least "decently different." But in another recent essay, Jim questions the staying power of today's high valuations. Read more here: Investing Legend: 'Higher Valuations Are Here to Stay'. Digging into Jim's biannual financial conference, Porter Stansberry shares a secret you can learn from big-name investors and their ideas. And he reveals all the details of Jim's special offer to attend this event, including which legends will be speaking next week. Read more here: The Most Unusual Gift We've Ever Offered. |

|

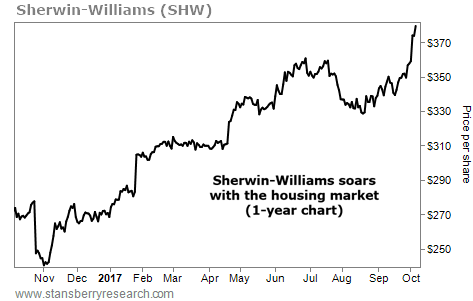

THIS REMODELING STOCK IS BOOMING WITH HOUSING

Today's chart highlights a company that rises with the housing market... As longtime DailyWealth readers know, Steve has been bullish on housing since the bottom of the bust. We've seen homebuilder stocks soar this year, including KB Home (KBH), PulteGroup (PHM), and NVR (NVR). And the housing market has done especially well in recent months. Home inventories are tightening, and prices are rising as a result. Right now, we're seeing another bullish sign – rising shares of paint company Sherwin-Williams (SHW). Founded in 1866, the company now has more than 4,000 stores throughout the U.S. Its paint brand has become a household name. Last year, Sherwin-Williams acquired competitor Valspar for about $11.3 billion. The two companies together drew about $15.8 billion in revenue for the year. Sherwin-Williams benefits when folks are building and remodeling their homes. And as you can see in the chart below, its stock is thriving... Shares have increased around 40% so far this year, putting the stock at new record highs. And if the housing market keeps making strides, this trend will likely continue... |

|

| Here's how to think about cash in your portfolio... Understanding cash is important, if often forgotten. Cash isn't a "do nothing" asset. It's future investment waiting for the right opportunity. Today, Dan Ferris explains why... |

Are You a

New Subscriber?

If you have recently subscribed to a Stansberry Research publication and are unsure about why you are receiving the DailyWealth (or any of our other free e-letters), click here for a full explanation... |

|

| It's Time to Bet Against the Canadian Dollar | | By Brett Eversole | | Thursday, October 5, 2017 |

| | The Canadian dollar has soared as much as 9% this year – which is a big move in the currency markets. |

| | How to Do Less... and Make More | | By Richard Smith | | Wednesday, October 4, 2017 |

| | Unfortunately, when it comes to investing, most people seem to want to "do more and make less." That, at least, is what the evidence suggests... |

| | Bitcoin Investors Are in a Frenzy – Proceed With Caution | | By Dr. Steve Sjuggerud | | Tuesday, October 3, 2017 |

| | I'm sure Teeka Tiwari was quizzed at the urinal last week... As I've said before, "When I can't even use the restroom in peace, I know we're at the top of the market." Here's what I mean... |

| | Investing Legend: 'Higher Valuations Are Here to Stay' | | By Jim Grant | | Monday, October 2, 2017 |

| | Jeremy Grantham has changed his mind. The question before the house is whether we should change ours, too. |

| | Porter's Latest Project Will Blow You Away | | By Justin Brill | | Saturday, September 30, 2017 |

| | The 2017 Stansberry Las Vegas Conference is in the books... |

|

|

|

|