Looking at NBJ’s Sports Nutrition and Weight Management category numbers, like those just published today in the Sports Nutrition and Weight Management Report, it often takes a moment of orientation. How could a $63.63 billion dietary supplement industry (preliminary numbers published recently in New Hope Network’s State of Natural Report) house a $69.86 billion SNWM industry? It takes little more than category definitions to clarify this. The Sports Nutrition and Weight Management categories include powerhouse functional food categories like meal replacements and nutrition bars and gels.

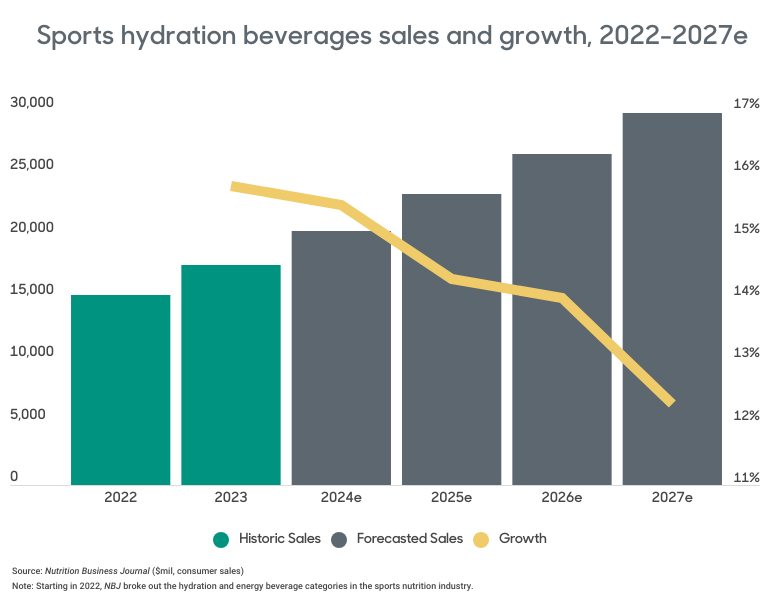

Well, and beverages. And this is the point at which head scratching returns. Beverages now account for more than two-thirds of the Sports Nutrition and Weight Management industry, and this consternation is less easily assuaged. First, there’s the relatively modest functional sports protein beverage sector, then the behemoth and double-digit-growing energy beverage sector, which itself accounts for more than one-third of the combined categories. But it’s the hydration beverage sector that is most astounding. At $17.65 billion, it is the second largest sector and the fastest growing, at 15.8% in 2023.

The head scratching may be accompanied, as it is among analysts and editors at NBJ, with the question: When did everyone get so thirsty? We’ve certainly seen it coming with high-profile acquisitions like Unilever’s purchase of Liquid IV and Néstle’s Nuun grab nine months later. New brands and formats—RTD or stick pack? Fizzy or non? More sugar or less? Other functional ingredients or straight hydration?—are still flooding the market, too. Consumers seem to be happily chugging away whether on epic road rides or just marathon Zoom meetings.

So, then follows the question, How long will they remain so thirsty? And the answer, according to NBJ is: As far as we can see. Growth is expected to taper only slightly in the coming years bringing hydration to just under 30% of the SNWM market share in 2027.

Cheers, and drink up! |