| Will You Outlive Your Money? | | By Dr. David Eifrig, editor, Retirement Millionaire | Wednesday, February 7, 2018

|

| In 1928, U.S. life expectancy was about 57 years.

Today, according to the Social Security Administration, folks turning 65 this year have an average life expectancy of 84.3 (men) or 86.6 (women). What's more, folks are living longer than ever. One in four 65-year-olds today will live past 90, and one in 10 will live past 95.

Most retirement plans assume you'll retire sometime around 65 and live for another 20 years.

But consider this...

Someone who is 65 years old today is expected to live 20 additional years... to the age of 85. But when this 65-year-old was born, scientists expected him to only live to the age of 68. So right now, this typical retiree is already 17 years "ahead of the curve."

And as medical advancements continue, that number could grow even more... even faster.

What does this mean for you?

Outliving one's retirement savings is the greatest fear of most people nearing retirement age. According to the Employee Benefit Research Institute, 61% of those aged 44 to 75 say running out of money in retirement is their biggest fear...

----------Recommended Links---------

---------------------------------

There's reason for that concern, too. More than half of Americans have less than $10,000 saved for retirement, according to GoBankingRates. And in an article in the New York Times, an economics professor estimated that nearly half of middle-class workers will be "poor or near poor" in retirement, living on a food budget of about $5 per day...

So imagine trying to milk those already sparse savings over 30 or 40 years.

This is why it's so crucial to estimate your lifespan and make sure you don't run out of money. Consider Social Security strategies, along with products like annuities and solid income-producing investments to provide a full, secure retirement.

But the first step to take is to develop a plan...

The retirement landscape has undergone vast changes over the past couple of decades...

As we already mentioned, people are living longer. And previously reliable sources of retirement income – like pension plans – are dying out.

That's where retirement planning comes in. There are three phases of retirement planning:

The accumulation phase is the time when you focus on growing your wealth and getting a general idea of how much money you'll need in retirement. You can do this through saving money, investing in the market, buying real estate, etc. It's never too early to start accumulating wealth. As we've said before, compounding is one of the most powerful tools you have to grow your wealth, especially when you've got time on your side.

During the consolidation phase, you should zero in on what you'll need to survive retirement... including bills you'll have to pay, income you expect to receive, etc. This is also the point when you switch to more conservative investments in order to preserve your capital. This phase is for people who are within several years of retiring.

In the final phase, you get to enjoy your hard work in retirement. This is when you begin taking distributions from income sources like Social Security, a pension (if you have one), dividend payments, etc.

Arguably the most important thing to do is to start accumulating wealth. Lots of Americans are relying on Social Security to get them through retirement. But the average monthly Social Security check in 2017 was only about $1,360.

And what will happen if Social Security goes bankrupt?

That's why you need to have a strategy to start building your nest egg. And the sooner you can start, the better.

One of the easiest ways to get started is buying shares of strong businesses that can keep up with future price changes and pass some of that growth back to investors. That's why for years, I've recommended people invest in what I call Sleep Well at Night ("SWAN") stocks.

These are investments that can pay you regular income – like dividend stocks, master limited partnerships (MLPs), real estate investment trusts (REITs), utilities, preferred shares, corporate bonds, and municipal bonds. If you're looking to make additional money in the market during retirement, these types of investments will not only provide you income now, but also set you up for income in the future.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Editor's note: Every month, Dave tells his Retirement Millionaire subscribers about safe ways to grow their income... debunks popular health myths... and shows them how to live a "millionaire lifestyle" for less. Get started with a risk-free trial subscription to Retirement Millionaire right here. |

Further Reading:

"'I'll start saving after I pay off my credit-card debt... after the kids are done with school... after I get that new job... after the next market correction,'" Dave writes. "If any of these sound familiar, you're shooting yourself in the foot." Get the hard truth here: How to Rescue Your Retirement in Four Easy Steps. Can you imagine safely making 15% or more per year on your investments? Dave showed DailyWealth readers why it's not too good to be true. Learn how here. |

|

THIS DEBT-RIDDEN COMPANY IS FLOUNDERING

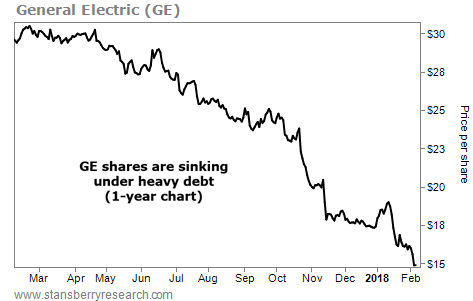

Today, we check in on one of Porter's often-repeated cautions... Porter frequently urges his readers to look at a potential investment's debt load – and to avoid companies with high and mounting debts. These businesses have problems brewing beneath the surface. And when troubled companies can't pay off their debts... defaults follow. A perfect example of this kind of downward spiral is industrial giant General Electric (GE)... Over the years, management has mortgaged GE's industrial assets – but not to reinvest in the company. Instead, it was financing credit cards at high interest rates. Worse, it has repeatedly sold off these securities just in time to prop up its quarterly earnings. Now, GE holds billions in financial assets of poor quality, financed by more than $130 billion in debt. And with a shrinking return on assets, this company has a world of trouble in store... As you can see in the chart below, this has taken a toll. Over the past year, shares fell nearly 50%. They are now at multiyear lows. It's more proof that debt-ridden companies make dangerous investments... |

|

| One of Dave's favorite long-term opportunities... If you're saving for retirement, you want to be in the market. And one of Dave's favorite businesses today could be a great long-term holding... |

Are You a

New Subscriber?

If you have recently subscribed to a Stansberry Research publication and are unsure about why you are receiving the DailyWealth (or any of our other free e-letters), click here for a full explanation... |

|

| One of the Few Cheap Investments in the World Today | | By Brett Eversole | | Tuesday, February 6, 2018 |

| | A certain part of the world hasn't offered today's value in more than 15 years. And it's in a strong uptrend as well... |

| | Not One, or Two, But FIVE Corrections of 10% Are Possible | | By Dr. Steve Sjuggerud | | Monday, February 5, 2018 |

| | OF COURSE a correction is coming! That is not a bold prediction. It is a simple fact... |

| | Here's the Latest on the Bull Market in Housing | | By Justin Brill | | Saturday, February 3, 2018 |

| | Is it time to start worrying about the housing market again? |

| | 'Buyer's Remorse' Is Losing You Money – Here's How to Beat It | | By Kim Iskyan | | Friday, February 2, 2018 |

| | Controlling these emotions can mean the difference between making a good investment... and one that you'll both regret and lose money on... |

| | How the Unemployment Rate Predicts Stock Market Crashes | | By Dr. Steve Sjuggerud | | Thursday, February 1, 2018 |

| | Jobless claims recently hit a 45-year low. And as stock investors, we can learn a ton from the unemployment rate... |

|

|

|

|